Seventy percent of the food consumed across the GCC travels through a single maritime chokepoint. That figure alone should keep procurement directors awake at night — and in early 2026, it became more than a theoretical risk. When maritime traffic through the Strait of Hormuz collapsed by nearly 97% following a series of military strikes in late February, food supply chains across the UAE, Saudi Arabia, Qatar, Bahrain, Kuwait, and Oman entered a crisis mode that no amount of prior scenario planning had fully prepared for.

Fertilizer shipments stalled. Perishable cargo sat stranded. Fresh produce prices jumped 4% almost immediately, while the broader food basket saw a 2.8% inflation spike driven by tariff pressure on top of logistics chaos. For a region that imports more than 85% of what it eats, this isn't a blip — it's a structural wake-up call.

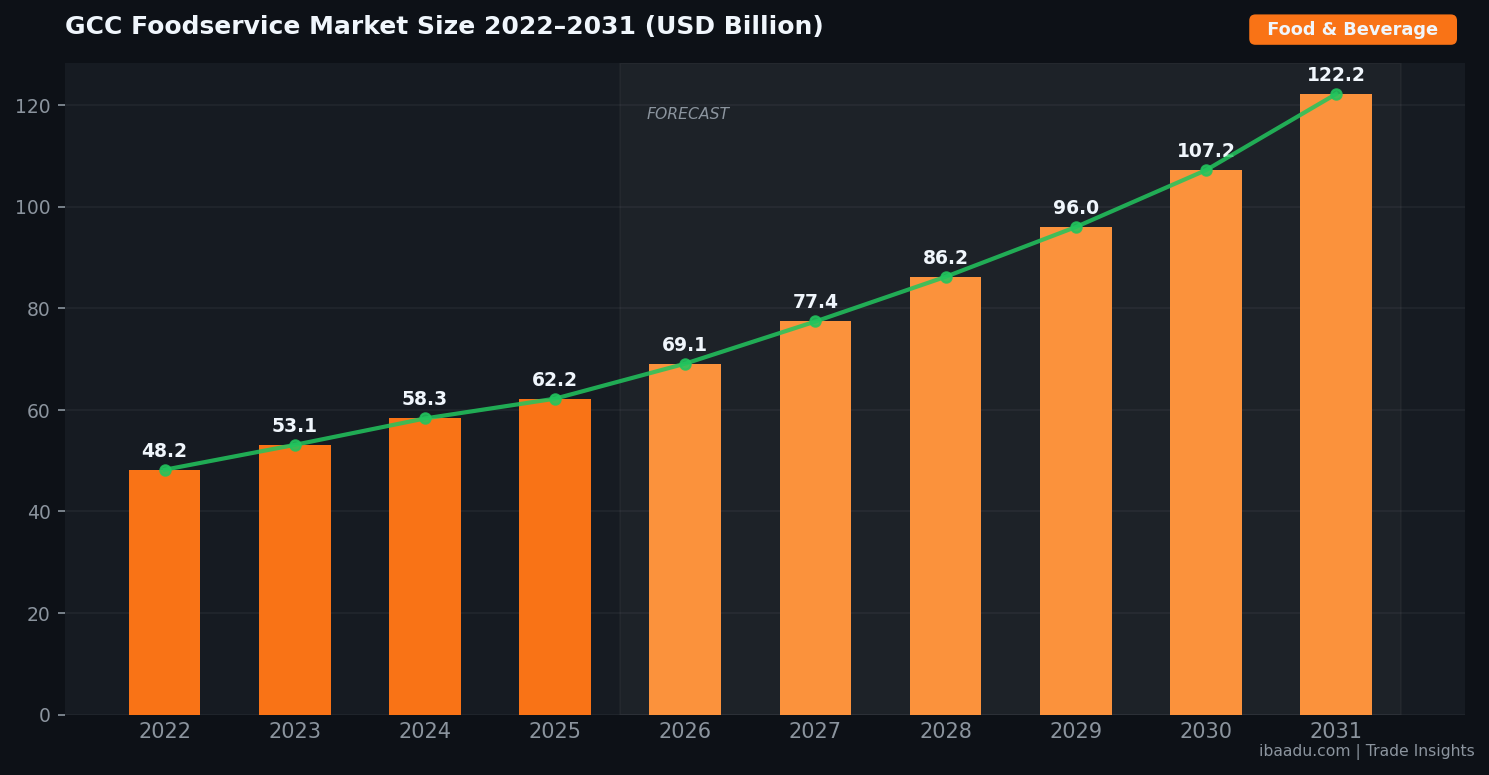

The GCC foodservice market was already on a powerful growth trajectory, valued at USD 62.2 billion in 2025 and projected to hit USD 122.2 billion by 2031 at a 12.07% CAGR (Mordor Intelligence). That growth creates enormous procurement opportunity — and enormous exposure. The procurement teams that come out of 2026 stronger are the ones who've already started moving from reactive sourcing to genuinely diversified, regionally anchored supplier networks.

The Hormuz Disruption: What It Means for Gulf Food Buyers

The Strait of Hormuz — just 21 miles wide at its narrowest — handles a disproportionate share of global energy and food trade for the Gulf region. When military action effectively shut down commercial traffic through it, the effects cascaded fast.

Roughly 3 to 4 million tonnes of fertilizer trade per month stalled, according to FAO estimates. The Gulf normally exports over 1.5 million tonnes of urea per month — supplies that feed agricultural operations across Asia and Africa. With that pipeline disrupted, global fertilizer prices rose 35% month-on-month to their highest in three years. That's not just an agricultural story; it's a forward signal for food commodity prices globally.

For procurement managers sourcing dairy, grains, packaged goods, and frozen proteins for Gulf distribution networks, the immediate operational reality was brutal. Lead times stretched. Buffer stocks that looked comfortable at 30 days felt dangerously thin at 15. Contracts with single-origin suppliers suddenly looked like liability rather than efficiency.

"We had 14 days of frozen protein stock when the Hormuz disruption hit. We needed 45. That gap is now non-negotiable in every supplier contract we sign." — Procurement director, UAE food distribution group (industry conversation, May 2026)

The immediate response from many buyers was to airfreight critical items — an expensive emergency measure, not a strategy. The smarter move, which more sophisticated procurement teams had already begun before February, is building genuine supplier redundancy across multiple shipping corridors. That means sourcing from Turkey, Egypt, Jordan, and India via Red Sea alternatives as well as from traditional European and Oceanian origins.

What's the practical implication? Any food and beverage buyer in the GCC who hasn't audited their single-origin exposures since Q1 2026 is carrying a risk their finance team doesn't fully see yet.

85% Import Dependency — The Structural Vulnerability

The 85% import figure isn't new. It's been the Gulf's food security reality for decades, driven by the simple physics of the region's arid climate and scarce freshwater. But the context around that number has shifted fundamentally.

The UAE imports over 85% of its food — some estimates put the country at closer to 90% for consumed calories. Kuwait sits at a similar level. Saudi Arabia, despite its Vision 2030 localization ambitions, still sources the majority of its food processing inputs from overseas. Even Qatar, which made significant investments in domestic food production following the 2017 blockade, remains heavily import-reliant for proteins and grains.

What's changed in 2026 is the convergence of multiple stress factors simultaneously. Tariffs matter here too. The 10% universal tariffs that have rippled through global trade have pushed food price inflation to 1.3% across the GCC in 2024, with 2026 shaping up worse. For procurement teams running tight margins in food distribution, hospitality, or institutional catering, that inflation translates directly to either absorbed losses or renegotiated supplier contracts.

There's a less-discussed dimension to this dependency that surprises even experienced procurement professionals: the GCC's food import reliance creates a multiplier effect on currency exposure. Most food commodity contracts are denominated in USD. When regional currencies experience any pressure — or when global dollar strength shifts — the landed cost of imported food inventory moves in ways that domestic-sourcing strategies buffer against. Procurement teams that have shifted even 15–20% of their volume to regional suppliers (Turkey, Jordan, Egypt, Oman's agricultural zones) have seen meaningful natural hedges against this currency volatility.

The UAE's National Food Security Strategy has set a target of 50% local agricultural production by 2051, and Saudi Arabia aims to localise 85% of its food processing by decade's end. These are aspirational timelines. The procurement reality today is that buyers can't wait for national strategies to mature — they need supplier diversification now, built from what's available regionally in 2026.

Supplier Diversification Strategies Procurement Teams Are Using Now

Diversification sounds obvious, but executing it under pressure — when your existing suppliers are struggling and your own inventory buffers are stretched — is genuinely difficult. Here's what the most effective procurement teams across the GCC are actually doing.

Multi-origin sourcing for key SKUs. For any product category representing more than 10% of food spend, procurement teams are now requiring a minimum of two active suppliers from geographically distinct origins. One European dairy supplier backed by one from New Zealand, for example, with a third from Turkey on standby terms. This isn't just contract language — it requires actively maintaining supplier relationships and regular qualification activities, not just paper agreements.

Regional supplier development. The MENA region has underutilised food production capacity in Turkey, Egypt, Jordan, and to a growing extent Morocco. Turkish food processors have scale and HACCP certification. Egyptian agribusiness has improved dramatically on quality standards. Procurement teams that have invested the time to qualify these suppliers over the past 18 months are now reaping the benefit. Those who didn't are scrambling.

Extended buffer stock commitments. The pandemic taught the GCC the value of strategic reserves for energy and PPE. The 2026 Hormuz disruption is teaching the same lesson for food. Major distributors and institutional buyers are now negotiating contracts that include mandatory minimum buffer stock provisions — typically 45–60 days of critical items — held either at supplier facilities or in bonded warehouses within the GCC itself. ibaadu.com connects buyers with verified regional suppliers who can fulfil these buffer arrangements from within the MENA supply base.

Corridor diversification. The Suez Canal route has historically handled much of the food trade flowing to the GCC from Europe. With Hormuz disrupted and Red Sea tensions creating alternative route premiums, procurement teams are now seriously evaluating the overland Turkey-to-Gulf corridor and direct air-sea combinations for perishables. DP World's logistics infrastructure at Jebel Ali remains a critical node — but the feeder networks supplying Jebel Ali are being actively rethought.

Spot market agility. Procurement teams that had previously locked all volume into long-term fixed contracts found themselves unable to pivot when primary suppliers failed in early 2026. The lesson: maintain 20–30% of volume on flexible or spot terms, even if unit costs are slightly higher. The optionality is worth the premium during disruption events.

How many of your current supplier contracts have a force majeure clause that was actually written with Hormuz in mind? If you're not sure, that's your starting point.

Joint GCC Procurement Programs and What They Get Right

One of the genuinely interesting structural responses to the 2026 disruption has been the acceleration of joint GCC procurement programs — coordinated buying across member states to achieve economies of scale and greater negotiating leverage with international suppliers.

Phase 1 of the GCC's emergency food security framework, running through 2026, specifically includes joint procurement mechanisms. This is significant because it represents a departure from the historically fragmented, country-by-country approach to food sourcing that has characterised the region. When six governments speak with one voice to a major grain exporter or protein supplier, the leverage dynamics change considerably.

For private sector procurement teams, there's an important lesson in the joint procurement model: aggregation works. Buyers who pool volume — even informally, through industry associations or purchasing cooperatives — gain access to pricing tiers and supplier attention that individual buyers simply can't achieve. This is particularly relevant in categories like packaged dry goods, cooking oils, and frozen proteins, where supplier minimum order quantities often disadvantage smaller distributors and hospitality operators.

The GCC's joint procurement initiative also includes a price monitoring function — systematic tracking of commodity price movements and early warning signals on supply constraints. Private sector procurement teams can build equivalent capability through commodity market subscriptions (MEED's monthly commodity trackers are useful) and through maintaining active conversations with multiple suppliers rather than relying on a single partner for market intelligence.

Phase 2 of the framework (2026–2028) pivots toward structural transformation: scaling domestic production, deepening regional agricultural integration, and building permanent strategic reserves. For procurement professionals, this signals where government investment will flow — and where supplier development opportunities will emerge. ibaadu's bulk procurement hub lists suppliers across GCC food categories who are actively seeking buyer partnerships under this framework.

Saudi Arabia's ambition to localise 85% of food processing by decade's end deserves specific attention. SABIC's involvement in agricultural inputs (fertilizers, packaging materials) and Aramco's peripheral exposure through agribusiness investments signal that the Kingdom is serious about backing these targets with capital. Procurement teams sourcing for Saudi-based operations should be mapping potential local supplier relationships now, ahead of the policy incentives that will make localisation commercially attractive.

Category Breakdown: Where the Supply Risk Is Highest

Not all food categories carry equal procurement risk in the current environment. Here's where experienced Gulf procurement professionals are concentrating their risk management attention.

Fresh produce. Highest volatility, shortest shelf life, most route-dependent. The 4% price increase seen immediately after the Hormuz disruption reflects how directly fresh produce procurement is exposed to shipping disruptions. The shift toward vertical farming and controlled-environment agriculture within the UAE (Bustanica at Dubai South produces 3 million kilograms of leafy greens annually) is reducing some exposure, but volume remains limited. Buyers sourcing fresh produce through ibaadu can access Jordanian and Egyptian agricultural suppliers with proven GCC export track records.

Proteins (frozen meat and poultry). Brazil, Australia, and India are the dominant origins for protein supply to the GCC. The Hormuz disruption hit Australian and Brazilian shipments routed via the Persian Gulf hardest. Indian protein exports via the Gulf of Oman maintained partial continuity. Procurement teams sourcing proteins are now actively qualifying Indian and Turkish suppliers as buffer origins, not just primary Australian and South American partners.

Grains and milling inputs. Saudi Arabia's SAGO (Strategic Grain Reserve Authority) holds significant wheat reserves — sufficient for months of domestic milling needs. But private sector buyers in hospitality, fast food, and industrial baking who source flour and grain derivatives directly are exposed to the same shipping disruptions. Procurement teams should know exactly how many days of grain-equivalent stock their key milling suppliers hold within the GCC, not just at origin.

Packaged dry goods and ambient products. Lower immediate disruption risk due to longer shelf life, but tariff exposure is higher here than in fresh categories. Many packaged food suppliers price in USD, meaning currency fluctuations translate directly to invoice volatility. Contracts with local GCC-based manufacturers — particularly in the UAE's KIZAD and SEZAD free zones, where significant packaged food manufacturing has been established — offer natural tariff and currency hedges that import-dependent supply chains don't.

Functional and health food categories. The GCC's functional food and beverage market is growing at 10.9% CAGR, reaching USD 20.18 billion in 2026 (Future Market Insights). This category is heavily import-dependent and increasingly under pressure from tariffs on supplements, specialty ingredients, and health-positioned packaged goods. Buyers in this space are particularly motivated to find regional formulation and contract manufacturing partners — a developing but real opportunity in the UAE and Saudi Arabia.

Source Verified Food & Beverage Suppliers Across the GCC

ibaadu connects Gulf food buyers with qualified regional and international suppliers — from fresh produce to packaged goods, proteins to specialty ingredients. Browse supplier profiles, request quotes, and negotiate directly.

Find Suppliers on ibaadu →Connecting Buyers to Verified Regional Suppliers

The fundamental procurement challenge the 2026 crisis has exposed isn't the shortage of suppliers globally — it's the shortage of qualified, verified regional suppliers that Gulf buyers have active relationships with. The Hormuz disruption didn't create a supply problem; it revealed that most procurement teams had never truly built their regional supply base beyond their primary global partnerships.

That's a fixable problem, but it requires active effort. Building a new supplier relationship from RFQ to qualified vendor typically takes three to six months when done properly — factory audits, quality testing, commercial terms negotiation, logistics trials. Doing that under crisis pressure, when you need product now, is brutal. The buyers who'll navigate the next disruption most effectively are those building those relationships now, during the relative stability of mid-2026.

Where do procurement teams in the Gulf find regional suppliers who are genuinely ready to supply at commercial scale? The traditional trade directory model doesn't work well for the Middle East — coverage is inconsistent and contact information is outdated. Trade shows like Gulfood (Dubai, annually in February) and Gulfood Manufacturing are excellent but limited in frequency. Industry associations like CIPS Middle East are useful for networking but not built for supplier discovery.

Digital B2B marketplaces purpose-built for the Middle East are filling that gap. ibaadu.com was designed specifically to connect verified suppliers across the GCC, Levant, and broader MENA region with qualified buyers across food and beverage, industrial, and construction categories. The platform lets buyers browse supplier profiles, view certifications, and initiate direct commercial conversations without the lead time of trade show cycles or the unreliability of cold outreach.

For food and beverage buyers specifically, ibaadu's supplier network includes distributors and manufacturers across the UAE, Saudi Arabia, Jordan, Egypt, and Turkey — the exact origins that regional procurement strategy should be prioritising in 2026. Whether you're sourcing ambient packaged goods, fresh produce, frozen proteins, or food service equipment, ibaadu's verified supplier listings provide a starting point that takes weeks off the qualification process.

Kuwait's procurement managers will note that the country has the fastest growth trajectory in the GCC foodservice market — a 13.89% CAGR through 2031 — making supplier network expansion particularly urgent for Kuwaiti food distributors and hospitality operators scaling alongside that market growth.

The GCC's food supply chain story in 2026 isn't really about the Hormuz disruption. That's a symptom. The story is about a region that has grown its food consumption economy to USD 62 billion and hasn't yet built the supplier infrastructure to match. The window to build that infrastructure proactively — rather than scrambling during the next crisis — is right now. Procurement teams that act in the next six months will have a meaningful competitive advantage over those who wait.

If your organisation is evaluating regional food and beverage suppliers in 2026, start your search on ibaadu.com. The platform's supplier verification process means you're reaching qualified partners, not unvetted listings.