In this article

Saudi Arabia's petrochemical sector — already responsible for roughly 80 percent of the GCC's chemical revenue and over USD 82 billion in annual output — is entering its most significant capacity expansion in more than a decade. In March 2025, the Saudi Ministry of Energy approved feedstock allocations for two major new complexes in Jubail, the kingdom's flagship petrochemical hub on the Eastern coast. Together, these projects will add more than five million tonnes per year of polymer and specialty chemical capacity by the end of the decade, reshaping supply dynamics for B2B buyers across the GCC and wider MENA region.

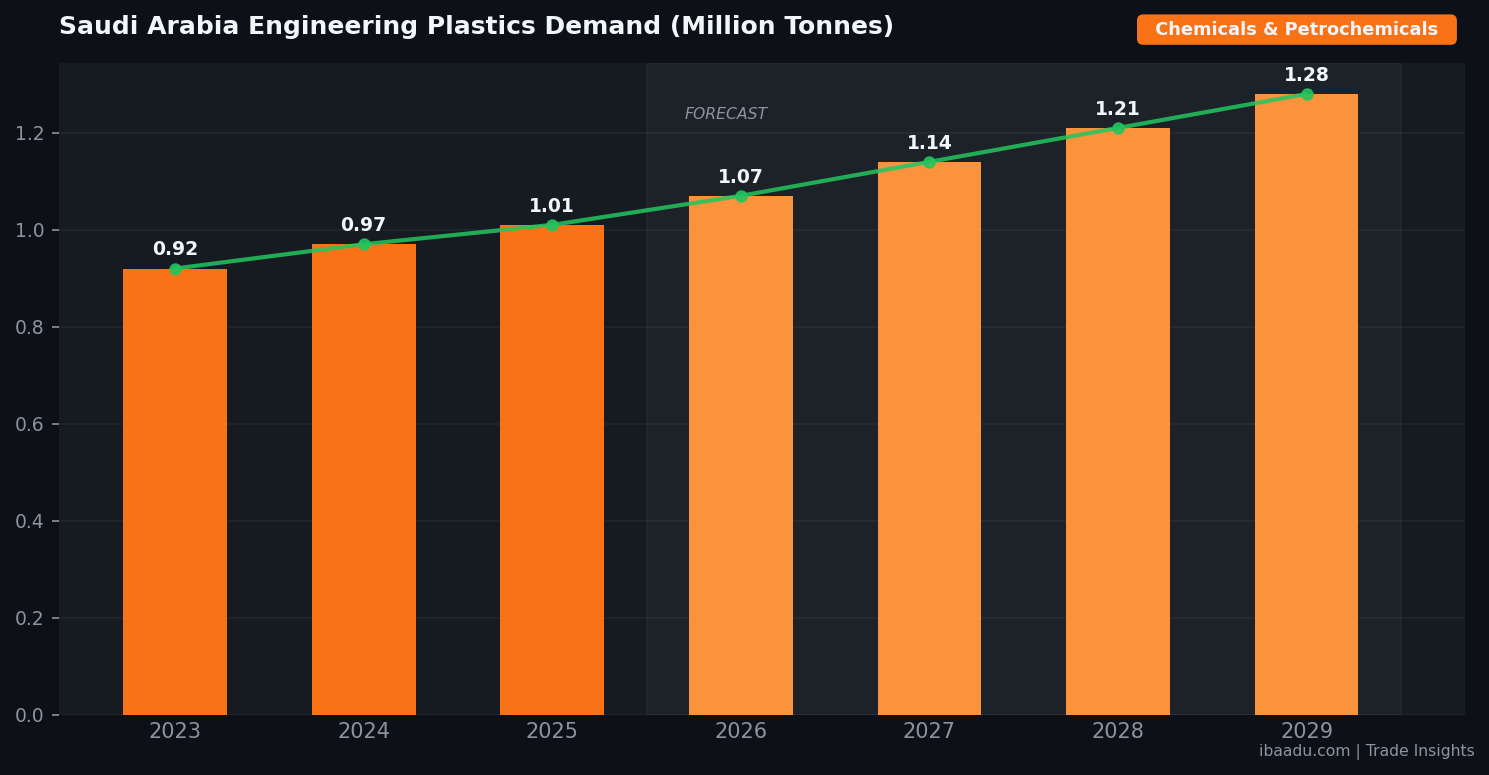

For procurement teams sourcing polyethylene, polypropylene, PVC, engineering plastics, and specialty chemicals from anywhere between Dubai and Cairo, this is not a distant story. The new Jubail capacity comes online against a backdrop of resilient domestic demand: Saudi engineering plastics consumption alone is forecast to grow from 1.01 million tonnes in 2025 to 1.42 million tonnes by 2031, a compound annual growth rate of nearly 5.8 percent. This Trade Insights briefing breaks down what's being built, when it lands, and how B2B buyers across the Gulf should structure their sourcing strategy in response.

The Jubail Expansion: Sipchem, LyondellBasell & Tasnee Unpacked

The first of the two Jubail projects is a joint venture between Saudi International Petrochemical Company (Sipchem) and US-based LyondellBasell. The complex centres on a mixed-feed steam cracker with a nameplate capacity of 1.5 million tonnes per year of ethylene, supported by downstream units that will produce around 1.8 million tonnes per year of finished polymers. The mixed-feed design — capable of swinging between ethane, propane, and naphtha depending on feedstock economics — is increasingly the standard configuration for new world-scale crackers in the Gulf, allowing operators to remain cost-competitive even when ethane allocations tighten.

The second project, led by National Industrialization Company (Tasnee), is even larger in tonnage terms. Tasnee received approval for a 3.3 million tonne per year integrated complex producing polyethylene, methyl tertiary butyl ether (MTBE), and a portfolio of specialty chemicals. The specialty component is particularly notable: Saudi Arabia has historically focused on commodity grades, but the Tasnee project signals a deliberate move up the value chain, targeting engineering plastics and additives that currently rely heavily on imports from Northeast Asia and Europe. Both projects are scheduled to reach mechanical completion between 2027 and 2028, with commercial start-up phased through 2028–2029.

Crucially, both projects are anchored in Jubail Industrial City — a deliberate choice that reflects the cluster economics underpinning Saudi petrochemical strategy. Co-location with existing crackers, utilities, and the King Fahd Industrial Port allows operators to share steam, hydrogen, and logistics infrastructure, lowering the capital intensity per tonne of installed capacity. For buyers, that translates into structurally lower production costs and a more predictable export programme out of the Arabian Gulf, with material reaching Jebel Ali, Sohar, Hamad, and Sokhna ports inside seven to ten days.

What 5 Million Tonnes of New Capacity Means for GCC Pricing

In the immediate term, regional polymer pricing remains largely flat. SABIC has continued to roll over its monthly contract prices for both polyethylene and polypropylene through the first half of 2026, reflecting balanced supply against steady downstream demand in construction, packaging, and converting. For buyers locked into quarterly or semi-annual purchase agreements, that stability has been welcome after two years of feedstock-driven volatility.

The pricing picture changes meaningfully once the new Jubail capacity begins to ramp. An additional five million tonnes of regional polymer output — even partly absorbed by export markets — will tighten the bid-offer spread on commodity grades and create real competitive pressure across GCC distributors. Buyers in the UAE, Qatar, Oman, and Kuwait should expect more aggressive pricing on linear low-density polyethylene (LLDPE), high-density polyethylene (HDPE), and polypropylene homopolymer grades from 2028 onward. Just as importantly, the specialty chemicals tranche from Tasnee should reduce the price premium and lead time on engineering plastics that currently flow from South Korea, Japan, and Germany.

Source Verified B2B Suppliers on ibaadu

Connect directly with Chemicals & Petrochemicals suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Downstream Winners: Construction, Automotive, Packaging & Solar

Several downstream sectors stand to benefit disproportionately from the new Jubail capacity. Construction remains the single largest end-market for Saudi polymers, with PVC pipes, HDPE geomembranes, polypropylene insulation, and expanded polystyrene tied directly to the kingdom's giga-project pipeline and the broader GCC infrastructure boom. With construction equipment demand alone projected to reach USD 9.24 billion across the GCC by 2030, the materials supply chain underneath those projects must scale in parallel.

Packaging, automotive, and electronics converters are the next tier of beneficiaries. The Tasnee specialty chemicals stream is expected to feed local production of polycarbonate compounds, ABS, polyamide grades, and engineering thermoplastics used in automotive interiors, white goods, and consumer electronics — categories where the Gulf currently imports the majority of finished resin. Renewable energy is the most under-discussed beneficiary: solar backsheets, ethylene-vinyl acetate (EVA) encapsulants, and cross-linked polyethylene (XLPE) cable insulation all draw heavily on the polymer chains being expanded in Jubail. With Saudi Arabia targeting 14 GW of new renewable awards in 2026 and the UAE pushing aggressive solar build-outs, polymer supply security has quietly become an energy procurement issue as well.

How GCC B2B Buyers Should Position for 2026–2028

The strategic playbook for procurement teams over the next two years has three elements. First, lock in baseline volumes on commodity polymers under flexible contracts that allow price renegotiation as new capacity enters the market. Buyers who tie themselves into rigid multi-year fixed-price agreements with single suppliers risk overpaying once the supply curve shifts in 2028. Second, qualify multiple suppliers in advance — both established producers like SABIC, Sipchem, Tasnee, Petro Rabigh, and SADARA, and the new joint-venture entities as they come online. Pre-qualifying lab samples, technical data sheets, and logistics windows in 2026 saves quarters of validation work later.

Third, treat engineering plastics and specialty chemicals as a strategic category, not a tactical one. As Saudi capacity moves up the value chain, buyers who source on price alone risk missing the formulation, technical service, and supply-continuity advantages that regional producers will offer. Engagement with local converters, masterbatch producers, and compounders — many of which list on B2B platforms such as ibaadu — provides a faster, more transparent route to qualified material than chasing global trader inventories. The buyers who build that relationship infrastructure now will be the ones with the lowest landed cost and the shortest lead times when the Jubail capacity wave breaks in 2028.

Finally, procurement leaders should pay close attention to sustainability and circularity requirements being written into Saudi and UAE downstream tenders. Recycled polyethylene content thresholds, low-carbon hydrogen-derived feedstocks, and mass-balance certification are increasingly being asked for in giga-project and packaging RFQs. Suppliers tied to the new Jubail complexes are positioning specifically around these requirements, and buyers who specify them early will see meaningfully better pricing and supply commitments than those that wait for compliance to become mandatory.

Frequently Asked Questions

How much new polymer capacity is Saudi Arabia adding through the Jubail complexes?

Combined, the new Sipchem-LyondellBasell joint venture and the Tasnee complex will add more than 5 million tonnes per year of polymer and specialty chemical capacity once fully operational, including 1.8mn t/yr of polymers from Sipchem-LyondellBasell and 3.3mn t/yr from Tasnee covering polyethylene, MTBE, and specialty chemicals.

What impact will the new Jubail capacity have on GCC polymer prices in 2026 and beyond?

In the short term — through 2026 — SABIC continues to roll over polyethylene and polypropylene contract prices, signalling balanced supply. Once the new Jubail crackers come online from 2028 onward, regional buyers should expect more competitive pricing on commodity grades and stronger availability of specialty engineering plastics inside the GCC.

Which sectors will benefit most from increased Saudi polymer supply?

Construction (PVC pipes, insulation, geomembranes), automotive (engineering plastics, polypropylene compounds), packaging (polyethylene film, PET), electronics, and renewable energy (solar backsheets, cable insulation) are the primary downstream beneficiaries. B2B buyers in these segments across the UAE, Egypt, Jordan, and the wider MENA region will see broader supplier choice and shorter lead times.

How can B2B buyers source petrochemicals and engineering plastics directly from Saudi producers?

Buyers can engage producers either through authorised regional distributors, direct contract negotiations for high-volume off-take, or via verified B2B marketplaces. Platforms like ibaadu connect GCC buyers with vetted suppliers across the petrochemical value chain — from base resin pr