In this article

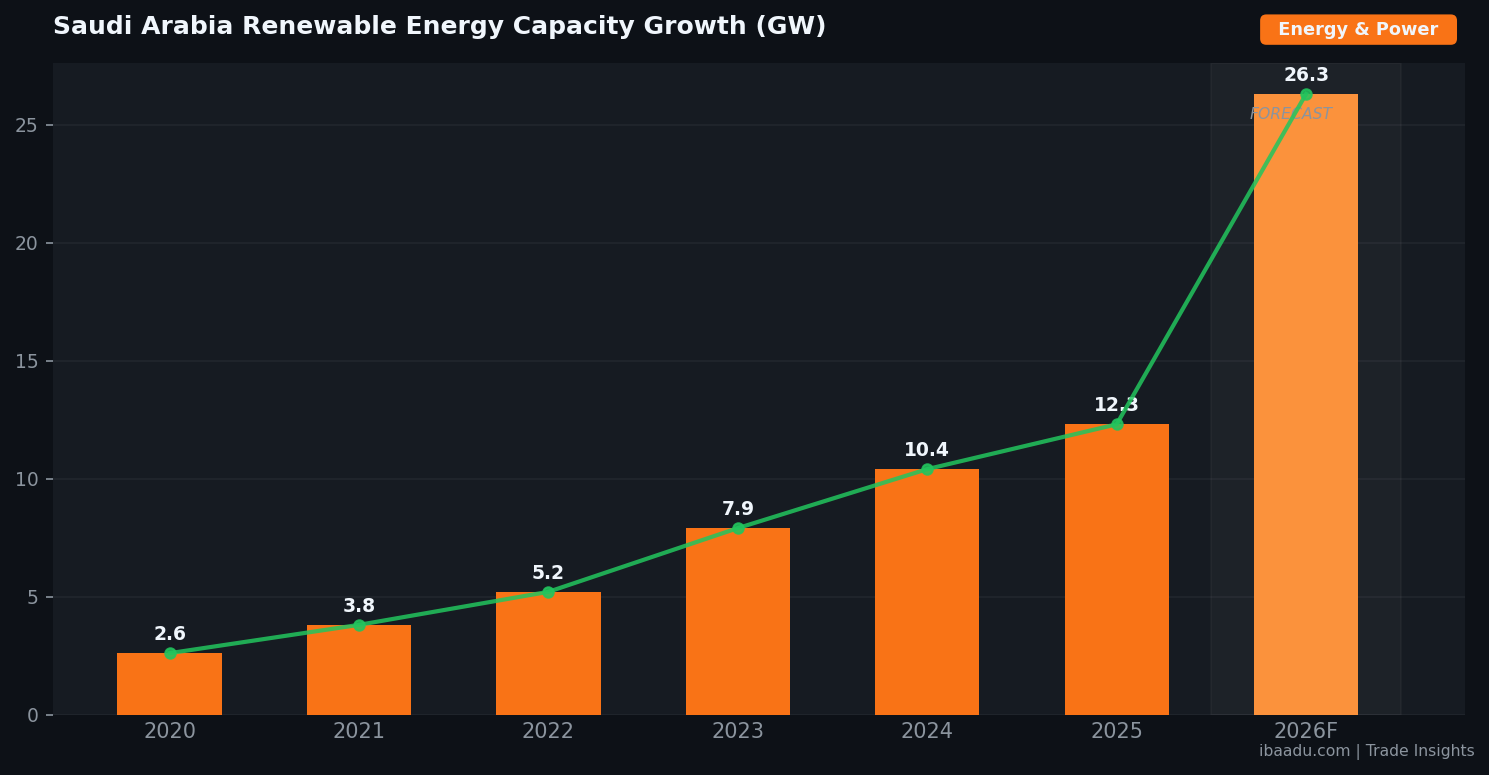

Saudi Arabia is executing the most ambitious renewable energy procurement programme in its history. With approximately 14 gigawatts of new solar and wind capacity set to be awarded through competitive tenders in 2026, the Kingdom is sending a clear signal to B2B buyers and suppliers across the GCC: the clean energy supply chain is open for business at an unprecedented scale. For procurement professionals, equipment manufacturers, and logistics providers, the window to position for this wave of contracts is now.

This surge is the direct result of Vision 2030's electricity diversification mandate, which sets a target of 50 percent renewable generation by 2030. With around 12.3 GW already connected to the national grid by end-2025, the 14 GW award round in 2026 would nearly double installed capacity in a single year. That kind of velocity creates compounding demand across dozens of upstream and downstream product categories — from solar modules and inverters to transmission cables, battery storage systems, and civil construction materials.

The Scale of Saudi Arabia's 2026 Renewable Procurement Programme

The Saudi Power Procurement Company (SPPC) has structured 2026 as a landmark year for clean energy contracting. Building on October 2025's award of five projects totalling 4.5 GW in a single transaction, the programme has demonstrated institutional capacity to execute at speed and scale. In 2026, SPPC is expected to issue tenders across utility-scale solar photovoltaic, onshore wind, and hybrid renewable-plus-storage configurations, with individual project sizes ranging from 300 MW to over 2 GW.

These projects are distributed across the Kingdom's key development corridors: the NEOM region in Tabuk, the NEON hydrogen economy cluster, Riyadh's expanding grid perimeter, the industrial cities of Jubail and Yanbu, and the Jazan economic zone in the southwest. Each corridor has distinct logistics requirements, infrastructure timelines, and preferred contractor relationships, meaning B2B suppliers need to map their positioning geographically, not just by product category.

The economic rationale for the programme is compelling. Saudi Arabia's power purchase agreement for wind energy reached a global record low of 1.33 cents per kWh in 2025 — a benchmark that reflects both competitive procurement discipline and the Kingdom's structural advantage in solar irradiation. As more capacity comes online, the domestic oil reserves currently consumed for electricity generation are freed up for export, generating incremental upstream revenue that funds ongoing Vision 2030 spending. For B2B buyers, this means government contract certainty and long-term off-take agreements that underpin supplier investment decisions.

The NEOM green hydrogen facility is expected to begin commercial operations in mid-2026, requiring 600 tonnes of clean hydrogen per day powered entirely by dedicated wind and solar assets. This facility alone represents a continuous procurement pipeline for electrolysis equipment, specialty gases, high-purity water treatment systems, and industrial instrumentation that will run for decades.

Key Product Categories and Supply Chain Opportunities

The 14 GW procurement round creates demand across a broad stack of equipment and services. Understanding which categories are in acute supply is essential for any procurement team or supplier entering this market. The primary hardware categories include monocrystalline and bifacial solar PV modules, single-axis tracking systems, central and string inverters rated for desert operating conditions, and high-voltage underground cables rated at 132 kV and above. Wind energy contracts will require nacelles, blades, tower sections, and foundation steel in quantities that most regional fabricators will struggle to fulfil without overseas partnerships.

Battery energy storage systems (BESS) are emerging as a critical co-procurement category. Saudi Arabia's grid management authority requires increasingly that large-scale renewable projects include storage capacity to smooth intermittency. Lithium iron phosphate (LFP) battery packs and the associated thermal management and fire suppression systems are in high demand, with lead times extending to 18 months from the major Chinese and Korean manufacturers. Regional distributors and engineering firms that can provide in-country stock and technical commissioning support will command significant pricing premiums.

Civil infrastructure procurement underpins every project. Structural steel for panel mounting, precast concrete for road access and cable trench covers, HDPE conduit for cable management, and geotextile materials for ground preparation are all consumed in enormous volumes on a gigawatt-scale solar site. Saudi contractors typically source 30 to 40 percent of civil materials locally under IKTVA requirements, creating structured opportunities for in-Kingdom fabricators and importers with bonded warehouse capabilities.

Operations and maintenance presents a longer-horizon procurement opportunity that B2B buyers frequently undervalue at the contracting stage. A 1 GW solar plant in Saudi Arabia will consume hundreds of tonnes of deionised water annually for panel cleaning, require periodic replacement of junction boxes, monitoring sensors, and inverter capacitors, and demand a continuous flow of personal protective equipment and specialist tools for the maintenance workforce. Suppliers who can establish framework supply agreements with EPC contractors at the project award stage will lock in multi-year revenue streams that outlast the construction phase.

Source Verified B2B Suppliers on ibaadu

Connect directly with Energy & Power suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Navigating Tender Processes and Local Content Requirements

Saudi Arabia's renewable energy tenders are administered by SPPC under the National Renewable Energy Programme (NREP), a framework overseen by the Ministry of Energy. The tender process follows a two-stage competitive model: a Request for Qualifications (RFQ) phase that establishes shortlisted developer consortia, followed by a Request for Proposals (RFP) phase where technical and commercial bids are evaluated. For B2B suppliers, the critical leverage point is the EPC contractor selection — because it is the EPC firm, not the developer, that issues subcontract and purchase orders for equipment and services.

The IKTVA (In-Kingdom Total Value Add) programme governs local content requirements across Saudi Aramco and affiliated energy projects, with a minimum local content threshold of 75 percent targeted across the energy sector by 2030. For renewable projects, SPPC applies a weighted scoring mechanism that rewards developer bids with higher proportions of locally produced or assembled content. This creates direct demand for Saudi-registered manufacturing entities and for GCC suppliers who can establish joint ventures or fabrication partnerships with Saudi companies.

Certification is non-negotiable for entering the Saudi energy supply chain. Solar module suppliers require IEC 61215 and IEC 61730 compliance, inverter manufacturers need IEC 62109 certification, and all electrical components must conform to SASO (Saudi Standards, Metrology and Quality Organization) product registration requirements. ISO 9001 quality management systems are a baseline expectation for any vendor seeking approved vendor list (AVL) status with major Saudi EPC contractors such as Alfanar, ACWA Power's engineering arm, and Saudi Aramco's project management subsidiaries.

For suppliers new to the Saudi market, the most efficient entry route is engagement with the Saudi Energy Efficiency Center (SEEC) and the Renewable Energy Project Development Office (REPDO), which maintain public databases of approved technologies and registered suppliers. Participation in SAFA (Saudi Arabia's Future of Aviation and Energy) and the Future Energy Summit in Abu Dhabi provides structured access to procurement decision-makers at SPPC, Saudi Electricity Company (SEC), and the major IPP developers active in the Kingdom.

Pricing Trends and Procurement Strategy for GCC Suppliers

The pricing environment for renewable energy components in the GCC is being shaped by three simultaneous forces: global module oversupply from Chinese manufacturers, tightening lead times on electrical balance-of-system components, and rising freight and insurance costs linked to regional logistics disruptions. Understanding how these dynamics interact is essential for GCC procurement teams setting 2026 budgets and for suppliers quoting on framework agreements.

Solar PV module prices dropped to historic lows in late 2024 and have stabilised in the range of USD 0.13 to 0.17 per watt peak for bifacial monocrystalline panels in GCC port delivery during early 2026. This pricing reflects sustained manufacturing overcapacity in China and Vietnam. However, panels certified for high-temperature and high-humidity operation — with specific low light performance ratings and extended warranty terms demanded by Saudi project owners — command a 15 to 25 percent premium over standard specifications. Procurement teams that specify only price will find themselves holding equipment that fails AVL compliance checks.

Transformer and cable markets tell a very different story. Global demand for high-voltage transformers has outpaced manufacturing capacity, with lead times for 132/33 kV units extending to 24 months from European and Japanese suppliers. Saudi projects drawing on 2026 tender awards will therefore need to initiate transformer procurement in Q3 2026 at the latest to maintain construction schedules targeting 2028 commissioning. GCC distributors who have placed forward orders with transformer manufacturers are in a strong negotiating position and should be proactively engaging with EPC procurement teams now.

For GCC B2B suppliers developing their 2026 positioning strategy, three approaches are generating the strongest results. First, establishing framework agreements with tier-one EPC contractors before project financial close, using pre-agreed pricing mechanisms that index to key commodity benchmarks. Second, offering vendor-managed inventory (VMI) services that reduce EPC procurement teams' administrative burden and create switching costs. Third, differentiating on technical support capability — the ability to provide commissioning engineers, O&M training, and warranty claims handling in-Kingdom is valued well above commodity price competition in the evaluation criteria of sophisticated buyers. B2B platforms that aggregate verified GCC suppliers by technical capability and certification status are increasingly used by procurement managers to short-list potential partners efficiently.

Frequently Asked Questions

How much renewable energy capacity is Saudi Arabia awarding in 2026?

Saudi Arabia's Saudi Power Procurement Company (SPPC) is set to award approximately 14 gigawatts of new solar and wind capacity through competitive tenders in 2026, representing one of the largest single-year clean energy procurement rounds globally.

Which product categories are in highest demand for Saudi Arabia's renewable energy projects?

The highest-demand categories include monocrystalline and bifacial solar PV modules, wind turbine components, high-voltage power cables and transformers, battery energy storage systems (BESS), SCADA and grid management software, and civil construction materials for plant infrastructure.

What certifications do B2B suppliers need to qualify for Saudi renewable energy tenders?

Suppliers typically need ISO 9001 quality management certification, IEC 61215 or IEC 61730 for solar modules, local content compliance under the IKTVA programme, and registration with SPPC or major EPC contractor approved vendor lists. SASO product certification is also required for most electrical components.

How can GCC-based B2B suppliers find buyers for renewable energy components in Saudi Arabia?

GCC-based suppliers can register on B2B procurement platforms like ibaadu.com to connect directly with developers and EPC contractors, attend sector events such as Future Energy Summit and SAFA, and engage with the Saudi Energy Efficiency Center (SEEC) for approved vendor programmes.

Conclusion

Saudi Arabia's 14 GW renewable energy procurement programme in 2026 is not a future opportunity — it is an active market event with timelines that are already running. B2B suppliers who align their certifications, local content strategy, and product specifications to SPPC and EPC contractor requirements in the next six months will be positioned to capture a share of one of the most significant infrastructure procurement cycles in the region's history. Whether you supply solar modules, high-voltage cables, BESS solutions, or civil construction materials, the demand signal from Riyadh is unambiguous. The question for every GCC procurement team and supplier is not whether to engage, but how quickly they can meet the technical and commercial threshold for entry.