In this article

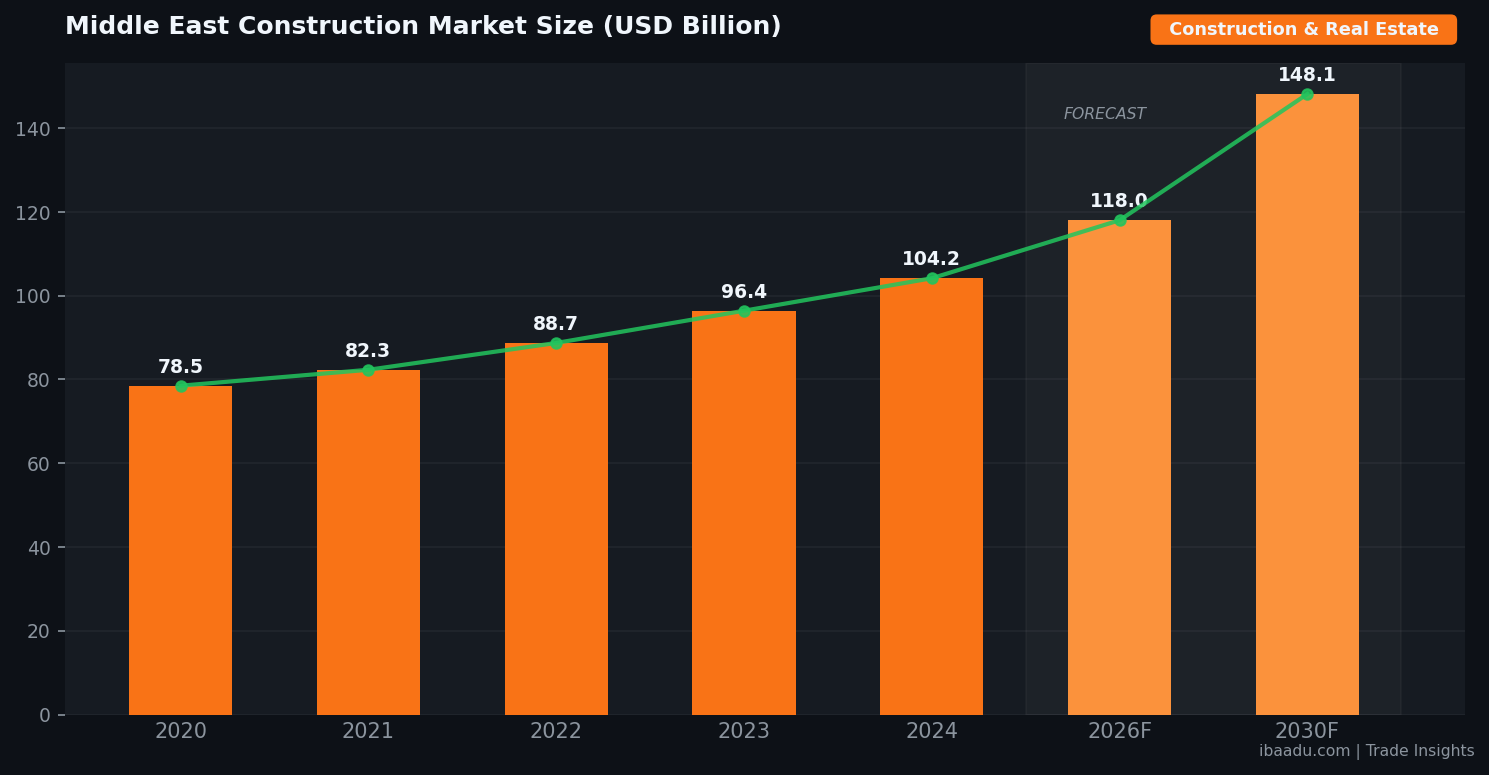

The Middle East's construction sector has entered a period of exceptional activity in 2026. Valued at approximately USD 104 billion in 2024, the regional market is now tracking well above that baseline — driven by simultaneous megaproject execution in Saudi Arabia and the UAE, both nations accelerating landmark infrastructure programmes that are unprecedented in scope. For B2B procurement professionals, manufacturers, and materials suppliers, this represents one of the most significant sourcing opportunities of the decade.

This Trade Insights report examines the structural forces behind the 2026 construction surge, identifies the specific project pipelines generating the greatest procurement volumes, and provides actionable guidance for suppliers seeking to qualify into GCC construction supply chains. Whether you supply steel, cement, structural aluminium, specialist equipment, or logistics services, understanding how demand is being distributed across the Gulf is essential to positioning your business effectively this year.

Market Scale: Why 2026 Is a Record Year for GCC Construction

The Middle East construction market is projected to grow at a compound annual growth rate of 5.89% through 2030, reaching USD 148 billion — but the pace of growth in 2026 specifically is outstripping earlier forecasts. Saudi Arabia's construction sector alone is expected to expand by an average of 5.4% per year through 2029, supported by a triple catalyst: Vision 2030 programme delivery, infrastructure preparation for Expo 2030 Riyadh, and early-stage groundwork for the 2034 FIFA World Cup.

In the UAE, the pipeline is equally ambitious. The USD 33 billion expansion of Al Maktoum International Airport — designed to eventually handle 260 million passengers annually — is one of the largest active construction programmes globally and is generating enormous downstream demand for steel, concrete, glazing, mechanical systems, and specialist subcontractors. Meanwhile, Abu Dhabi continues to invest heavily in industrial zones, mixed-use real estate, and transport corridors linking Emirate districts to the Saudi border.

What distinguishes 2026 from previous boom cycles is the convergence of these programmes with a deliberate regional push toward procurement localisation. Saudi Arabia's Vision 2030 framework explicitly mandates higher in-country value (ICV) thresholds, incentivising contractors to source from GCC-based suppliers wherever possible. For regional manufacturers and distributors, this creates a structural tailwind that is likely to persist through at least 2030. The shift from volume-led procurement to performance-led procurement — where contractors evaluate suppliers on delivery reliability, sustainability credentials, and digital documentation capability — is also reshaping how supply chains are being structured.

Key Projects Driving Materials Procurement Volumes

While the aggregate market figures are impressive, procurement opportunities are concentrated in a handful of flagship programmes that are currently at peak execution phase. NEOM, the USD 500 billion linear city development in northwest Saudi Arabia, remains the single largest source of specialist construction procurement in the region. In 2026, the NEOM programme is advancing multiple sub-projects simultaneously — including THE LINE's infrastructure backbone, Sindalah Island hospitality development, and the OXAGON floating industrial port — each requiring dedicated supply chains for structural steel, advanced glass, modular components, and heavy machinery.

The Riyadh Metro, now operational across several lines, has catalysed a secondary wave of construction along its corridors, with mixed-use residential and commercial towers being developed by both public and private developers keen to capitalise on improved connectivity. This has translated into sustained demand for ready-mix concrete, interior fit-out materials, MEP systems, and facade cladding — categories where international suppliers with regional distribution capacity are finding strong traction.

In Qatar, post-World Cup infrastructure maintenance and the development of new economic zones along the Saudi border are sustaining procurement activity that might otherwise have wound down. Oman's National Programme for Enhancing Economic Diversification (Tanfeedh) is funding port expansions at Sohar and Duqm, both of which require significant civil engineering materials and marine construction equipment. Kuwait's Northern Gateway project — a planned city to house two million people north of Kuwait City — is entering detailed design and early procurement phases, with tender activity expected to intensify through 2027.

Egypt, while outside the GCC proper, is increasingly integrated into the regional construction supply chain through the New Administrative Capital project and the Suez Canal Economic Zone expansion. Egyptian manufacturers of steel, ceramics, and construction chemicals are actively competing for GCC contracts, adding another dimension to the competitive landscape that regional buyers need to monitor.

Source Verified B2B Suppliers on ibaadu

Connect directly with Construction & Real Estate suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Supply Chain Pressures and How Buyers Are Responding

The scale and simultaneity of active construction programmes across the region is creating measurable strain on materials supply chains. Steel rebar, one of the most fundamental inputs in large-scale civil and structural construction, has experienced intermittent availability pressures through early 2026, driven partly by global trade policy shifts — including tariff changes affecting steel imports from key producing nations — and partly by the sheer volume of demand being absorbed by Saudi and UAE projects at the same time. Buyers with long-term framework agreements and approved vendor rosters are significantly better positioned than those operating on spot procurement.

Cement and ready-mix concrete represent another pressure point. Both Saudi Arabia and the UAE have invested in expanding domestic production capacity, but peak programme execution is testing the limits of that capacity in specific regions. Logistics, rather than raw production volume, is often the binding constraint: delivering materials to remote giga-project sites in the Tabuk and Hail regions of Saudi Arabia requires dedicated supply chain infrastructure that many smaller suppliers have struggled to establish independently.

Leading contractors are responding with several strategic adaptations. Procurement teams are extending visibility windows — issuing framework tenders for two and three year supply agreements rather than project-by-project spot buying. Digital procurement platforms and vendor management systems are being deployed to standardise supplier qualification, compliance documentation, and performance tracking. There is also a growing emphasis on sustainability credentials: embodied carbon reporting, circular materials strategies, and low-carbon cement alternatives are moving from aspirational to mandatory in many tender specifications, reflecting both regulatory direction and client ESG commitments.

For international suppliers assessing entry into the GCC market, the message is clear: compete on consistency, compliance, and documented performance rather than price alone. Contractors managing multi-billion dollar programmes cannot afford supply disruptions; a supplier that can demonstrate reliable delivery schedules, robust quality management, and responsive technical support will command a premium over cheaper but less dependable alternatives.

Opportunities for B2B Suppliers: Entering the GCC Construction Market

The breadth of the GCC construction boom means that procurement opportunities exist across virtually every materials and equipment category — but the mechanisms for accessing those opportunities differ significantly between project types and client organisations. For suppliers new to the Gulf market, understanding these mechanisms is as important as product competitiveness.

Tier-1 international contractors operating in the region — including firms from Europe, South Korea, China, and Turkey — manage their own approved vendor lists (AVLs) and pre-qualification programmes. Getting onto an AVL requires submitting detailed technical documentation, financial accounts, quality certifications (ISO 9001 is a baseline; ISO 14001 and OHSAS 18001 are increasingly expected), and references from comparable projects. The process typically takes three to six months for initial approval, making early engagement critical for suppliers targeting 2026 and 2027 procurement windows.

For smaller and mid-sized contractors — particularly those executing residential, commercial, and fit-out projects in the UAE and Saudi Arabia — B2B trade platforms provide a faster and more accessible route to market. These platforms allow suppliers to present their product catalogues, certifications, and pricing structures to a curated audience of qualified buyers without the overhead of maintaining a full in-market sales presence. ibaadu serves exactly this function for the GCC region, connecting verified suppliers and manufacturers with procurement professionals across the Gulf.

Categories with particularly strong near-term demand in 2026 include: structural steel and rebar (especially suppliers able to serve remote site locations), specialist geotechnical and foundation equipment, fire protection and MEP systems, external cladding and facade systems, modular bathroom and kitchen units for the hospitality sector, and sustainable building materials such as recycled aggregate, low-carbon concrete additives, and high-performance insulation. Suppliers in these segments who can demonstrate GCC-relevant experience, regional logistics capability, and competitive lead times are well positioned to convert enquiries into long-term framework partnerships.

Frequently Asked Questions

What materials are most in demand for GCC construction projects in 2026?

Steel rebar, structural steel, cement, ready-mix concrete, and aluminium cladding are the highest-demand materials in 2026. Demand is concentrated in Saudi Arabia's giga-projects and UAE megaprojects such as Al Maktoum Airport expansion, driving procurement volumes to record levels.

How can international suppliers enter the Saudi and UAE construction supply chain?

International suppliers typically qualify through contractor pre-qualification programmes, industry trade platforms such as ibaadu, and direct engagement with Tier-1 contractors. Saudi Aramco, NEOM, and the UAE's major developers all publish vendor registration portals. Having ISO certification and demonstrable GCC project references significantly improves acceptance rates.

What are the biggest procurement risks in the Middle East construction sector?

The main risks include payment delays on large government-backed contracts, price volatility for imported materials (especially steel), logistics bottlenecks at major ports, and last-minute scope changes on giga-projects. Buyers should build buffer stock and negotiate price-escalation clauses for multi-year supply agreements.

Is the Middle East construction market expected to keep growing after 2026?

Yes. Industry forecasts project the Middle East construction market to reach USD 148 billion by 2030, fuelled by Saudi Expo 2030, the FIFA 2034 World Cup infrastructure, and continued UAE urban expansion. Procurement demand for building materials, plant, and equipment is expected to remain elevated through at least 2030.

Conclusion

The Middle East construction sector in 2026 represents a convergence of scale, urgency, and structural reform that has few precedents in the region's commercial history. Saudi Arabia and the UAE are executing the most ambitious built-environment programmes of their respective histories simultaneously — and the procurement demand this generates cascades across every materials category, equipment segment, and service discipline in the construction value chain. For B2B suppliers prepared to invest in proper qualification, regional logistics capability, and compliance documentation, the GCC construction boom offers a durable pipeline of business that is likely to extend well into the next decade. The window to establish supply relationships at programme inception — when contractors are still building out their approved vendor rosters — remains open, but it is narrowing as projects move from design into peak execution.