GCC Construction Materials Market Value (USD Billion), 2021–2028. Sources: Mordor Intelligence, Grand View Research, ibaadu Trade Insights. 2026 onwards = forecast.

Walk the procurement floors of a major Dubai contractor today, and you'll find something that wasn't there two years ago: organised chaos. Not disorganisation — the opposite of it. Procurement teams are managing more concurrent material streams, more vendor conversations, and more project-specific specifications than any previous cycle has required. This isn't a spike. It's a structural shift, and understanding why it's happening is the first step for any supplier or buyer trying to navigate it.

The headline numbers are striking enough. Saudi Arabia's construction materials market reached USD 55.6 billion in 2025 and is tracking toward USD 86.3 billion by 2034 at a 5% compound annual growth rate, according to Mordor Intelligence. But those figures undersell what's actually happening at the transaction level. The Vision 2030 programme has created a procurement environment where the Kingdom isn't just building more — it's building things the region has never built before. NEOM's The Line, a 170km linear city designed for 9 million residents, requires construction specifications that didn't exist as procurement categories three years ago. Specialized acoustic panels, ultra-high-performance concrete, solar-integrated cladding systems: these aren't off-the-shelf items that a procurement manager can source from the usual roster of approved vendors.

At the same time, the UAE continues to expand on a parallel track. Dubai's Urban Master Plan 2040 is adding 134 square kilometres of urban area. Abu Dhabi's pipeline includes over 600 infrastructure and real estate projects valued at more than AED 1.2 trillion. The Yas Island expansion, Saadiyat Cultural District and the ongoing build-out of logistics zones around KIZAD and Khalifa Port are generating procurement volumes that have stretched lead times on several key materials by eight to twelve weeks compared to 2024 baselines.

The Qatar post-World Cup period was widely expected to produce a slowdown in GCC construction. It didn't — the momentum transferred. Oman's Duqm Special Economic Zone and the Port of Duqm development are absorbing significant materials demand. Kuwait's long-delayed South Silk City project appears to be advancing through procurement phases. Even Bahrain, with its smaller footprint, is consuming elevated volumes of structural steel for the Bahrain Bay expansion.

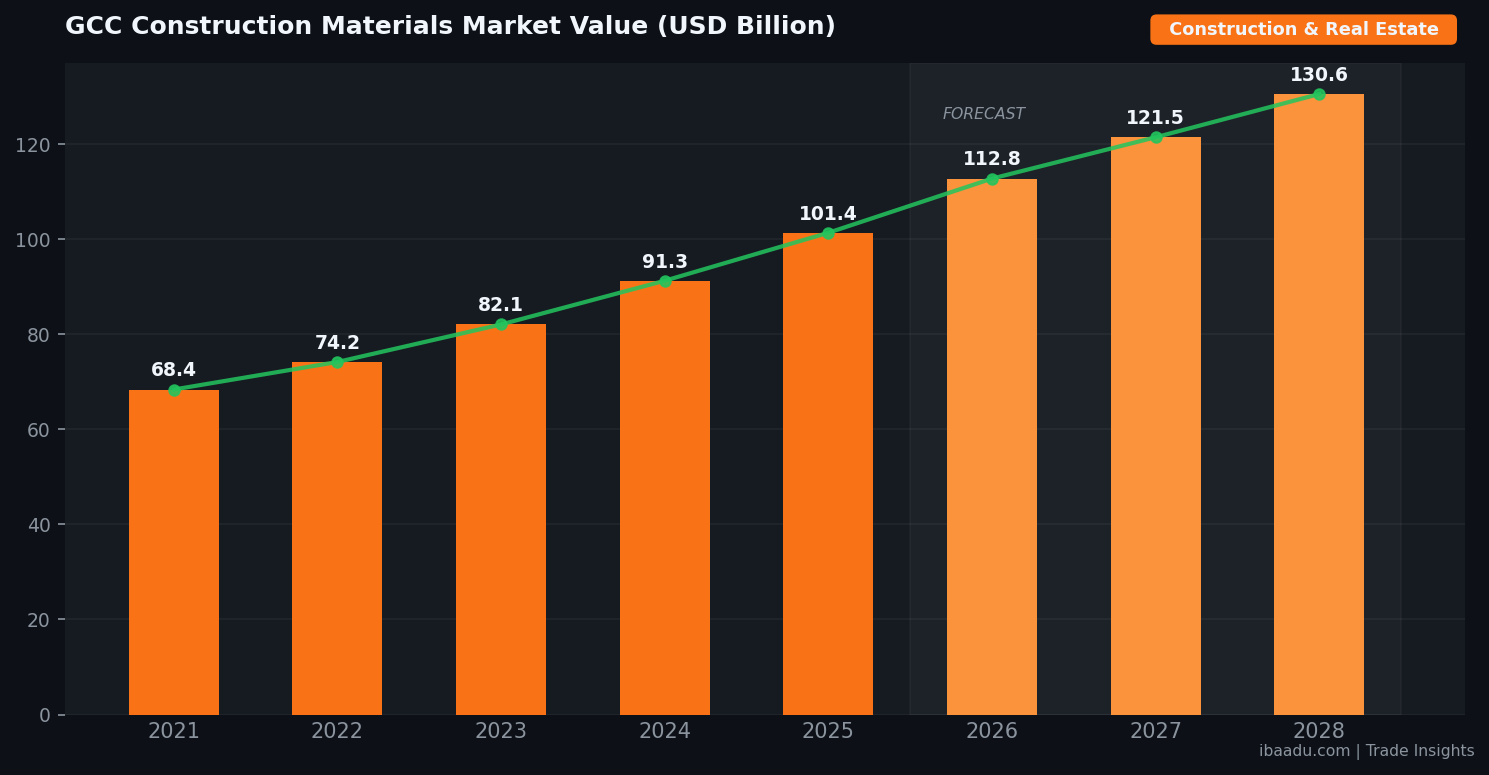

The result is a GCC construction materials market that Grand View Research and multiple regional analysts now value at USD 112.8 billion for 2026 — a figure that represents approximately 34% growth from the 2021 baseline of USD 68.4 billion. Buyers and sellers operating in this market aren't working in the same conditions they understood just three years ago.

Construction materials procurement in the Gulf tends to be discussed as though it were monolithic. It isn't. The steel, cement, and aggregates markets each operate on different supply dynamics, different lead time patterns, and different risk profiles. Getting procurement strategy right means treating them separately.

Saudi Arabia's Vision 2030 projects are consuming over 8 million metric tons of rebar and structural sections annually, a figure that has pushed domestic producers — Emirates Steel (now part of EMSTEEL), Conares, and Hamriyah Steel in the UAE; Al Rajhi Steel, Hadeed (a SABIC subsidiary) and Al Ittefaq Steel in the Kingdom — to their effective capacity ceilings. The consequence for procurement teams is straightforward: those who rely on spot purchasing are routinely paying a 12–18% premium over contract buyers, and they're still waiting longer. If you don't have a frame agreement with at least one regional mill, you're operating at a structural disadvantage in the current market.

The more interesting dynamic is the import side. Turkish and Chinese rebar, which historically provided a pricing buffer, has become a complicated equation. Anti-dumping measures in Saudi Arabia have added cost to Turkish imports. Chinese steel's price competitiveness remains strong, but lead times from Chinese mills — given the length of the supply chain and current port congestion at Jeddah Islamic Port — can run to sixteen weeks from order confirmation. For fast-cycle projects, that's untenable.

Quality certification is another pressure point that doesn't get enough attention in procurement conversations. Saudi Aramco, Emaar, and ADNOC all maintain preferred vendor lists with specific mill certifications as mandatory requirements. A material that meets generic ISO standards but lacks project-specific Mill Test Reports will be rejected on site. Procurement teams sourcing from new vendors — regional or international — need to build the certification verification process into their lead time assumptions, not treat it as an afterthought.

GCC cement demand at 115.86 million tons in 2026 represents a market where domestic production capacity is under genuine strain for the first time in over a decade. Saudi Arabia alone has over a dozen cement producers — Arabian Cement, Saudi Cement, Yanbu Cement — but plant maintenance scheduling, clinker availability, and logistics bottlenecks have combined to create regional shortages in specific grades. Sulphate-resistant cement, required for foundations in coastal and high-salinity environments, has seen spot prices in some GCC sub-markets rise by 22% year-over-year through Q1 2026.

Ready-mix concrete procurement is where the complexity compounds. Most major UAE projects now specify self-compacting concrete (SCC) or high-performance concrete (HPC) mixes for structural elements. These aren't available from every batching plant — and the batching plants that can produce them are running at extended turnaround cycles. Early engagement with concrete suppliers — twelve weeks or more before pour dates on major pours — is no longer best practice; it's the minimum viable approach.

This is the category that surprises even experienced procurement professionals: the most constrained material in the current GCC cycle isn't a high-specification product. It's crushed stone aggregate. The UAE's position as a net importer of aggregates means that aggregate pricing in the Emirates is structurally linked to maritime freight rates, which have been elevated and volatile since 2024. For any project consuming more than 50,000 tonnes of aggregate, securing supply early — and ideally with a volume-linked price schedule — is the difference between hitting the project budget and blowing it.

The supply chain challenges in GCC construction procurement in 2026 don't come from a single source. They're layered, and they interact with each other in ways that linear risk frameworks don't capture well.

Port congestion is the most visible layer. Jebel Ali — still the ninth-largest container port in the world and the largest in the Middle East — has been operating at elevated utilisation since late 2024. DP World has added berth capacity, but the speed at which project cargo volumes have grown across the GCC has outpaced infrastructure expansion. Average dwell times for project cargo at Jebel Ali have increased by three to five days compared to 2023 norms, according to CIPS regional data. For a project running on tight float, those days matter.

Inflation in key material categories is the second pressure. Steel prices in the GCC spot market remain above long-run averages. Aluminium — a critical input for curtain wall systems, window frames, and cladding — has been affected by both global commodity dynamics and the energy cost of primary aluminium smelting. The UAE's own Emirates Global Aluminium (DUBAL/EMAL) is among the world's most cost-efficient aluminium producers, but their output is largely committed to long-term contracts with major fabricators. Spot buyers are facing structural price premiums.

Workforce constraints are the supply chain bottleneck that procurement teams are least equipped to solve directly, but most affected by. Labour shortages in skilled trades — welders, formwork carpenters, MEP technicians — have created productivity drags that translate directly into extended demand for temporary materials and site equipment. A project that was planned on a 14-month delivery timeline is now being executed over 18 months in many cases, which extends the procurement cycle, stretches storage requirements, and creates secondary demand for materials that were originally on-hire rather than purchased.

How do you manage this environment? The procurement professionals getting it right in 2026 share three common practices: they've moved to 18–24 month procurement planning horizons for Category A materials; they've diversified their vendor base across a minimum of three approved suppliers per major material category; and they've invested in digital procurement tools that give them real-time visibility into vendor lead times, open orders, and price benchmark data.

Connect with 200+ verified UAE and GCC wholesale suppliers of steel, cement, aggregates, aluminium and MEP materials. Post your procurement request and receive competitive quotes within 24 hours.

Browse Construction Suppliers →For most of the past two decades, construction materials procurement in the Gulf operated on relationship infrastructure: an approved vendor list, a handful of established rep firms, and a phone-based quotation process that rewarded incumbency over competitiveness. That model is breaking down — not because relationships have become less important, but because the volume and complexity of procurement in the current cycle has outgrown what relationship-based systems can handle.

MEED's analysis of the 2026 Gulf construction market identifies digital procurement adoption as one of the three forces — alongside AI-assisted price forecasting and modular construction — that will distinguish project winners from losers in the current cycle. The contractors and developers who've moved procurement to digital platforms are seeing measurable outcomes: Gulf Business research from Q1 2026 puts the average savings from digitally-run tender processes in the 8–14% range versus paper-based equivalent processes, with a reduction in procurement cycle time from quote request to order confirmation of approximately 40%.

What does digital procurement actually look like on the ground? For large main contractors — the Arabtecs, Binnies, and Consolidated Contractors International Company (CCC) equivalents of the world — it means ERP-integrated procurement modules with supplier portals, automated approval workflows, and spend analytics dashboards. For mid-tier contractors and project developers, it's increasingly meaning B2B procurement platforms that aggregate verified supplier networks and enable competitive quotation without the need for a purpose-built system.

Platforms like ibaadu.com are filling exactly this gap in the GCC market. The ability to post a Procurement Request Quote (PRQ) to hundreds of verified regional vendors simultaneously — and to receive structured, comparable responses within 24 hours — is a procurement capability that simply didn't exist for mid-market buyers three years ago. It's the kind of tool that lets a project procurement manager source an alternative aggregates vendor when their primary supplier hits a capacity constraint, or find a certified structural steel trader who can commit to a specific Mill Test Report standard, without spending two weeks working through a network of contacts.

The AI dimension is emerging rather than mature in Gulf construction procurement, but the direction of travel is clear. Early applications focus on price trend analysis (using historical purchase data to identify optimal ordering windows for volatile commodities like steel and aluminium), supplier performance scoring (integrating delivery performance data into vendor qualification decisions), and demand forecasting (using project programme data to generate forward procurement requirements before they become urgent). SABIC and Aramco are already deploying AI procurement tools internally; the question is how quickly that capability cascades down to their contractor and supplier ecosystems.

It's tempting to treat the GCC construction market as a single entity. In practice, the UAE and Saudi Arabia — the two dominant procurement markets — operate on different rhythms, different vendor relationship dynamics, and different regulatory frameworks. Procurement strategies that work well in one market often need meaningful adaptation for the other.

The UAE market is characterised by its diversity and speed. With over 200 nationalities participating in the economy and a procurement culture shaped by the free zones (KIZAD, Jebel Ali Free Zone, Dubai Multi Commodities Centre), the Emirates has developed a procurement ecosystem that's genuinely international. A contractor in Dubai thinks nothing of sourcing structural steel from Turkey, facade systems from Germany, MEP equipment from India, and fit-out materials from China — often within the same project. The speed expectation is high: the concept of a 30-day procurement lead time for standard materials is increasingly treated as a failure condition rather than an acceptable norm.

Saudi Arabia's procurement reality is shaped differently. Saudisation (Nitaqat) requirements mean that procurement decisions have workforce implications beyond the materials themselves. The preference for In-Kingdom Value Add (IKVA) — essentially a local content requirement — has increased the strategic importance of domestic suppliers and in-country manufacturing partnerships. A vendor who can demonstrate meaningful Saudi manufacturing presence or local value addition has a material advantage over a pure trading or import operation in competitive tender situations. This is reshaping the vendor landscape: international suppliers who've historically served the Saudi market from UAE-based trading operations are investing in Kingdom-based finishing, fabrication, or distribution infrastructure to maintain competitiveness.

The payment cycle reality also differs. UAE project payment terms — even with recent regulatory improvements — average 65–90 days for materials suppliers on major private-sector projects. Saudi government projects, historically much slower, have improved significantly through the Monshaat SME payment protection framework and the Etimad platform for government procurement, but 120-day terms remain common in practice. Suppliers managing cash flow across both markets need to model these dynamics into their pricing and working capital strategies.

What does this mean for buyers sourcing across the GCC? It means that a single approved vendor list doesn't travel. The vendor who's your preferred steel trader in Dubai may not be competitive in Riyadh once logistics, local content requirements, and payment risk are factored in. Building a market-specific vendor panel — with regional coverage in both the UAE and KSA — is a procurement infrastructure investment that pays for itself in the first major cross-border project.

The practical question that every procurement manager in Gulf construction is wrestling with right now isn't abstract: how do you build a vendor panel that performs in a market characterised by capacity constraints, price volatility, and compressed delivery timelines? The answer isn't complicated, but it does require deliberate structure.

Not all vendors warrant the same relationship investment. A tiering framework — Tier 1 (strategic partners with frame agreements and volume commitments), Tier 2 (qualified alternates with active relationships but no volume guarantees), Tier 3 (catalogue contacts for spot procurement) — gives procurement teams clarity about where to invest relationship time and where to use transactional tools. Most mid-tier GCC contractors have this inverted: they invest heavily in managing a large number of Tier 3 relationships because they haven't done the work to elevate their best vendors to Tier 1 status.

Fixed-price contracts for volatile commodity categories are often unacceptable to suppliers in the current market, but that doesn't mean you're stuck with fully open-ended exposure. Index-linked pricing agreements — where materials prices are tied to a published commodity index (London Metal Exchange for aluminium and copper, CRU for steel rebar) with an agreed base price and cap on upward movement — give both parties workable protection. More Gulf developers and contractors need to be negotiating these mechanisms as a standard contract feature rather than treating them as exotic arrangements.

Supply chain risk in the GCC construction market in 2026 comes most frequently from a single point of failure: a primary vendor who hits a capacity constraint, a quality failure, or a financial difficulty, with no pre-qualified alternative in place. The procurement cost of qualifying a backup vendor — typically two to four weeks of sampling, testing, and administrative approval — is trivially small compared to the project cost of a six-week gap in materials supply. Systematic alternate vendor qualification for every Category A material should be a procurement standard, not an optional enhancement.

The relationship-based procurement model has a structural blind spot: it systematically undervalues vendors you don't already know. A regional B2B procurement platform like ibaadu.com provides access to a pre-verified vendor database that covers construction materials, industrial supplies, and trade goods across the UAE, Saudi Arabia, Qatar, Oman and the wider GCC. For procurement managers who've been working from the same approved vendor list for three years, a structured vendor discovery exercise on a platform like this can identify qualified alternates in 48 hours that would take weeks to surface through traditional network channels.

The GCC construction materials market in 2026 rewards procurement teams who've done the structural work — the vendor development, the pricing framework design, the digital tooling adoption — ahead of when they need it. The project pipeline is real, the demand is sustained, and the supply chain constraints aren't going away quickly. That combination is exactly the environment where preparation is the competitive advantage.

Vision 2030 mega-projects in Saudi Arabia — including NEOM, The Line, Diriyah Gate and the Red Sea Project — combined with UAE infrastructure programmes are generating unprecedented procurement volumes. GCC cement demand is projected to hit 115.86 million tons in 2026, while the combined construction materials market is valued at over USD 112 billion.

Structural steel, cement, aggregates, aluminium profiles, glass, and prefabricated modular components are the highest-demand categories. Saudi Arabia's Vision 2030 projects alone are consuming over 8 million metric tons of rebar and structural sections annually.

ibaadu.com is a dedicated B2B trade marketplace for the Middle East that connects contractors, developers and procurement teams with verified regional suppliers. Buyers can post procurement requests and receive competitive quotes from multiple vendors within 24 hours.

Lead time compression, price volatility in steel and cement, port congestion at Jebel Ali and Dammam, and the concentration of procurement within a small number of large contractors are the primary pain points.

Whether you're sourcing rebar, cement, aggregates, aluminium profiles or MEP materials across the UAE and GCC — ibaadu connects you with verified regional suppliers who can deliver to your project specifications.

Post a procurement request at ibaadu.com and receive competitive quotes within 24 hours. Or reach us directly on WhatsApp to discuss your project requirements.

WhatsApp: +971 58 597 8602