In This Report

- The $182 Billion Opportunity — and the Procurement Headache Behind It

- Which Equipment Categories Are Moving Fastest

- Hormuz Disruptions and What Smart Buyers Are Doing Differently

- Saudi Arabia vs. UAE: Two Very Different Procurement Environments

- Sourcing Strategies That Are Actually Working in 2026

- Why Regional B2B Platforms Are Becoming the Default Tool

The $182 Billion Opportunity — and the Procurement Headache Behind It

GCC cement demand hit 115.86 million tons this year. That single figure tells you more about the pressure facing regional procurement teams than any boardroom strategy document. The Gulf's construction machine isn't slowing down — if anything, it's accelerating into a wall of supply constraints that nobody fully anticipated when Vision 2030 was announced.

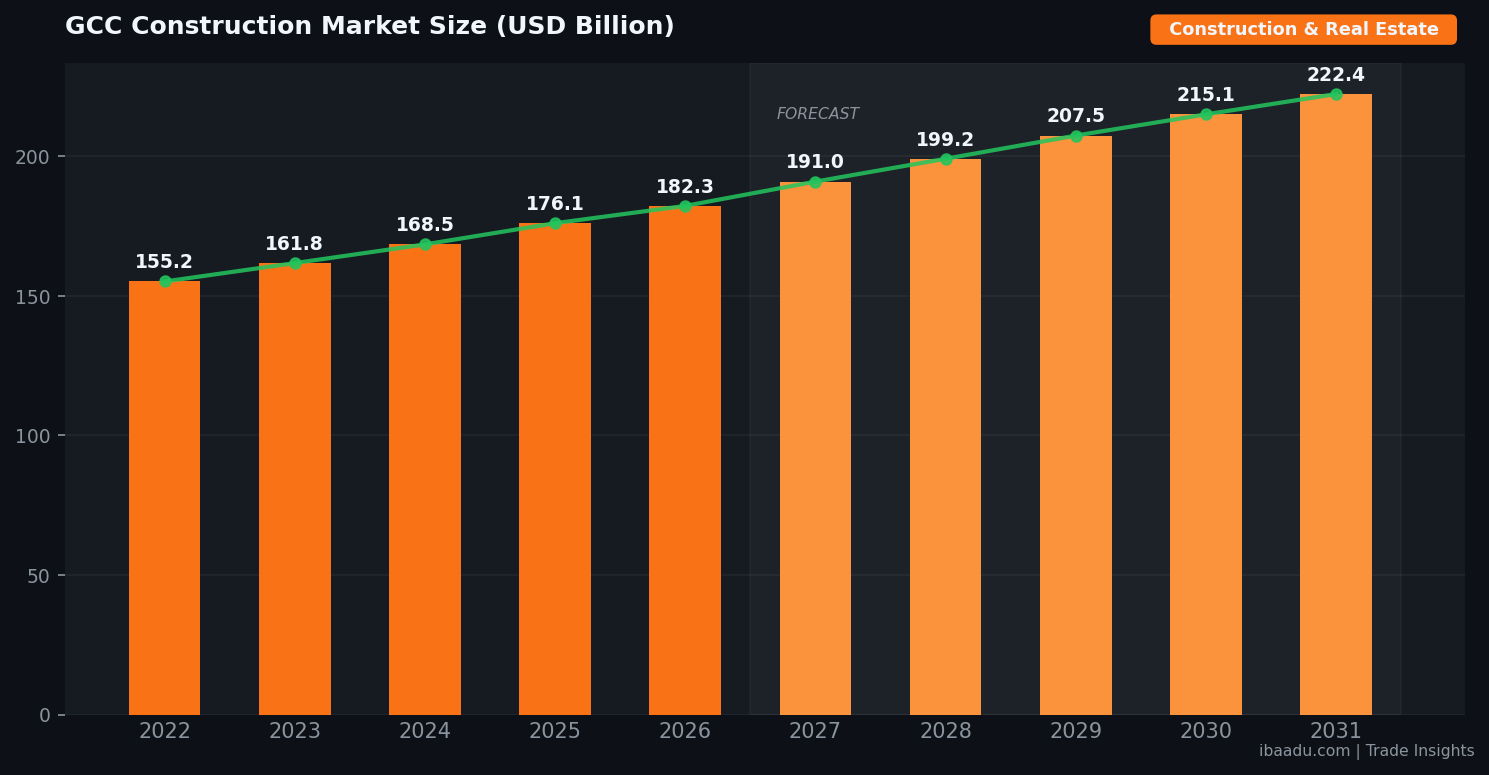

The GCC construction market is valued at USD 182.34 billion in 2026, according to Mordor Intelligence, with Saudi Arabia accounting for 45.62% of that figure and posting the fastest national CAGR at 5.36%. These aren't just headline numbers. They translate directly into equipment orders, material tenders, logistics contracts, and sourcing decisions that procurement managers across the Gulf are navigating daily — often without the supplier visibility they need.

Here's what doesn't get discussed enough: the construction surge isn't evenly distributed. Mega-projects like NEOM, Diriyah Gate, and Abu Dhabi's Reem Island developments are consuming equipment at rates that are distorting the regional market. Tower crane lead times that ran eight to twelve weeks in 2023 are now sitting at twenty to twenty-eight weeks for specific configurations. Concrete pump availability in the Riyadh and Dammam corridors has tightened considerably. And that's before you factor in what's happening with the Strait of Hormuz.

The macro story is compelling. The micro reality — finding a verified supplier of 80-tonne rough terrain cranes in Jeddah, or sourcing formwork systems for a 47-storey residential tower in Dubai with a 6-week delivery requirement — is where most procurement professionals spend their days. And it's that gap between market opportunity and sourcing execution that's reshaping how Gulf construction buyers operate in 2026.

If you're running procurement for a tier-1 or tier-2 contractor in the GCC, you already know the challenge. The question is whether your sourcing infrastructure has kept pace with the project pipeline you're trying to deliver.

Which Equipment Categories Are Moving Fastest

Not all construction equipment is under the same pressure. Understanding which categories are genuinely tight — and which ones just feel tight because of poor supplier visibility — is one of the more valuable distinctions a procurement professional can make right now.

The GCC construction machinery market is valued at USD 7.3 billion in 2026, growing at a 5.68% CAGR toward USD 9.62 billion by 2031 (Mordor Intelligence). But within that aggregate, the distribution is uneven.

Earthmoving and Excavation: Excavators and bulldozers remain the highest-volume category. Saudi Arabia's infrastructure construction sector — growing at 5.63% CAGR on the back of transport and utility programs — is absorbing significant excavator supply. Chinese OEM brands like XCMG and SANY have captured meaningful market share by offering shorter lead times and flexible financing structures that European competitors haven't matched. Don't underestimate this shift — it's structural, not cyclical.

Lifting Equipment: Tower cranes and mobile cranes are where procurement teams are feeling the most acute pain. The concentration of high-rise construction in Dubai's Jumeirah Village Circle corridor and Riyadh's diplomatic and financial districts has created localised shortages. There are verified suppliers in the GCC with available inventory, but many aren't reachable through traditional tender databases. Browse crane and lifting equipment suppliers on ibaadu to access regional availability directly.

Concrete Equipment: Batching plants, transit mixers, and concrete pumps are under sustained demand pressure. With GCC cement consumption at 115.86 million tons this year, the downstream concrete processing equipment market has tightened proportionally. Qatar's post-World Cup commercial development pipeline and Bahrain's Northern City reclamation project are both contributing to regional demand.

Safety and Scaffolding Systems: This is the category most buyers underestimate. Modular scaffolding systems — particularly the ring-lock and cup-lock varieties used on complex facades and high-rise cores — have delivery lead times that are now affecting project schedules. UAE contractors working on large mixed-use developments have started placing longer-horizon orders, sometimes 16 to 20 weeks out, to protect programme milestones.

Power Generation: Temporary power for construction sites — diesel generators and increasingly hybrid solar-diesel units — is a category where regional suppliers have invested significantly. ADNOC's downstream development sites and KIZAD's industrial zone expansions both rely heavily on temporary power infrastructure, and the shift toward hybrid units is accelerating as contractors face both environmental reporting requirements and fuel cost pressures.

The pattern across all these categories is the same: supply exists in the market, but it's not always visible to buyers through the channels they've traditionally used. Tender portals and established vendor lists don't update fast enough to reflect real-time availability. That's a sourcing problem, not a supply problem.

Hormuz Disruptions and What Smart Buyers Are Doing Differently

Let's be direct about what's happening with the Strait of Hormuz. The disruptions affecting Gulf shipping routes in 2026 are not a temporary inconvenience — they're a structural stress test on procurement models that were built for a more predictable world.

Importers sourcing construction equipment and materials via Hormuz-routed shipping are now renegotiating long-standing supplier contracts to add secondary sources from India, Southeast Asia, and East Africa. Port delays that averaged four to six days in early 2024 are now running twelve to eighteen days in the worst months. For a construction programme with tight milestone deadlines, an eighteen-day delay on a tower crane or a structural steel shipment isn't an inconvenience — it's a contractual liability.

Here's the piece that surprises even experienced Gulf procurement professionals: the disruption is affecting regional suppliers differently based on where their own supply chains originate. A UAE-based equipment dealer whose inventory arrives via Singapore and Malaysian ports may have significantly shorter delay exposure than a competitor importing directly from European manufacturers via Suez. Your supplier's supply chain matters as much as your own.

What are smart buyers actually doing? The playbook that's emerging looks like this:

First, they're diversifying supplier geographies within the region. Rather than single-sourcing a product category from one national market, they're qualifying two or three suppliers across UAE, Saudi Arabia, and Oman to reduce concentration risk. Second, they're pre-positioning critical items. Strategic inventory pre-positioning — holding six to eight weeks of high-critical items on-site rather than the traditional two to three — has become standard practice on large civil infrastructure projects. Third, they're building direct relationships with regional distributors rather than relying on international OEM sales teams who are often disconnected from actual in-region stock levels.

The fourth strategy is less obvious: they're using B2B discovery platforms to identify suppliers they didn't know existed. The Gulf market has significant supplier depth that traditional procurement networks don't surface. Explore verified construction material suppliers across the GCC on ibaadu and you'll find regional distributors with in-stock inventory that simply don't appear in tender portals.

DP World's Jebel Ali continues to be the most resilient entry point for construction equipment imports — its infrastructure, customs integration, and bonded warehousing capabilities give it a meaningful advantage during periods of wider port disruption. But even Jebel Ali isn't immune to cascading delays when upstream shipping routes are under pressure. The procurement teams performing best right now are those who've built flexibility into their sourcing model rather than optimising purely for unit cost.

Saudi Arabia vs. UAE: Two Very Different Procurement Environments

Anyone who tells you GCC procurement is a single market has probably never sat in both a Riyadh tender committee and a Dubai procurement meeting in the same week. The differences are substantial, and they affect sourcing strategy in ways that don't show up in headline market data.

Saudi Arabia is the larger market, the faster-growing market, and the more complex procurement environment. Vision 2030's construction pipeline — anchored by NEOM (even at its revised scope), Diriyah Gate, King Salman Park, the New Murabba development, and dozens of secondary infrastructure programmes — has created a procurement ecosystem that runs on multiple parallel tracks simultaneously.

The giga-project track operates with dedicated procurement teams, international tender processes, and direct OEM relationships that bypass traditional channel structures. The secondary infrastructure track — roads, utilities, schools, hospitals — runs through the Ministry of Municipal and Rural Affairs with established local contractor networks. And the private sector track — commercial real estate, logistics parks, industrial zones — operates with more flexibility but also with greater dependence on finding the right regional suppliers quickly.

SABIC's downstream investment in Jubail and ARAMCO's offshore fabrication requirements create additional demand layers that affect equipment availability throughout the Eastern Province. When both SABIC and a large civil contractor are competing for the same inventory of industrial-grade generator sets, the procurement team with stronger regional supplier relationships wins.

The SABER certification requirement for construction equipment entering Saudi Arabia is also creating differentiation. Suppliers who've completed SABER registration for their key product lines can deliver significantly faster than those who haven't — and many regional buyers don't ask about SABER status early enough in the supplier qualification process. By the time customs delays materialise, the project schedule has already taken the hit.

The UAE runs a different procurement culture. Speed is rewarded. Decision cycles on procurement that would take twelve weeks in the Saudi public sector often complete in four to six weeks in Dubai's private sector. Dubai Customs' integration with DP World's systems at Jebel Ali creates one of the smoothest import processes in the region — but it rewards suppliers who have their documentation and certification in order before the cargo arrives.

KIZAD in Abu Dhabi and Dubai's various free zones have become important staging and storage locations for construction equipment serving both UAE and export markets. Suppliers based in KIZAD or JAFZA have measurable logistics advantages over those operating from outside the UAE, particularly when buyers need just-in-time delivery to active construction sites.

The UAE market also has deeper penetration of digital procurement tools — e-procurement platforms, digital tender portals, and B2B marketplaces are more routinely used than in Saudi Arabia. That's partly cultural and partly structural: the UAE's smaller geography means procurement teams can practically visit any supplier in a half-day, so digital discovery is valued for breadth rather than just proximity. Find UAE-based construction suppliers on ibaadu with verified profiles and direct contact details.

Sourcing Strategies That Are Actually Working in 2026

After over a decade tracking procurement patterns in the Gulf, the sourcing approaches that consistently outperform are rarely the most technically sophisticated. They're the ones built on better information and stronger regional relationships than the competition.

Here's what's separating high-performing procurement teams from the rest right now:

Extending the qualified vendor list beyond tier-1 defaults. Most GCC construction procurement functions maintain vendor lists that were built during lower-volume periods. Those lists reflect the suppliers you knew then, not the full range of suppliers that exist now. The regional market has matured significantly — there are well-capitalised distributors in Oman, Jordan, and Egypt who can serve GCC projects competitively on price and lead time but who aren't on most procurement shortlists. Building that broader network before you need it is the difference between having options and scrambling.

Treating supplier financial health as a procurement variable. The construction industry's payment cycle is under stress. Projects that are delayed for regulatory or design reasons don't stop consuming cash — they just delay the payments that suppliers need to stay liquid. A supplier who was healthy in 2023 may be carrying significant receivables pressure in 2026. Procurement teams that qualify suppliers on financial health as rigorously as they do on technical capability are protecting their project schedules, not just their audit files.

Using category-specific market intelligence rather than general commodity indices. Tower crane rental rates in Dubai don't move with the same dynamics as concrete pump prices in Riyadh. Trying to negotiate either using a general materials cost index is a mistake. The Gulf market has enough depth that category-specific intelligence — obtained through direct supplier conversations, regional trade reports from MEED and Gulf Business, or B2B platform data — is both available and valuable.

Getting upstream of the tender. The procurement professionals consistently producing the best outcomes in the Gulf construction market are the ones who engage with the supplier market before the formal tender process begins. Understanding what's available, at what lead time, from which geographic points — that intelligence shapes the specifications and timelines that go into the tender. Coming to the market cold after the spec is locked is the most expensive way to source anything.

Leveraging regional B2B platforms for supplier discovery, not just price comparison. There's a tendency to think of B2B platforms purely as price tools — a way to benchmark quotes. The more valuable use in the GCC market is discovery: finding suppliers you didn't know existed who have verified credentials, regional experience, and available capacity. Search industrial and construction equipment vendors across the Middle East on ibaadu with category filters, country coverage, and direct contact access.

Why Regional B2B Platforms Are Becoming the Default Tool

The procurement landscape in the GCC has historically been relationship-dependent in a way that's both a strength and a vulnerability. Strong relationships with a small number of trusted suppliers work well — until those suppliers can't deliver, their prices move out of range, or their capacity is absorbed by a bigger contract elsewhere.

What's shifting in 2026 is the recognition that relationship depth and market breadth aren't mutually exclusive. The best procurement teams are maintaining their core supplier relationships while simultaneously building access to a wider regional network through B2B discovery platforms. It's not either/or — it's both.

Global B2B platforms have struggled to serve the Middle East construction market well. The product categories don't match regional specifications. The suppliers listed are often outside the region with uncompetitive lead times. And the trade compliance requirements — SABER certification, Dubai Municipality approvals, local content requirements under Iktva in Saudi Arabia — aren't reflected in supplier profiles.

Regional platforms built for the GCC market close that gap. ibaadu.com operates specifically as a Middle East B2B trade marketplace, connecting construction buyers across the UAE, Saudi Arabia, Qatar, Oman, Kuwait, Bahrain, Jordan, and Egypt with verified regional suppliers. The supplier profiles are built around GCC-relevant credentials — not generic global certifications that don't map to what regional buyers actually need to know.

Does it work for procurement at scale? Yes — and the use case isn't just SME buyers finding their first regional supplier. Tier-1 and tier-2 contractors are using regional B2B platforms for specific sourcing gaps: categories where their existing vendor list is thin, geographies where they don't have established contacts, or product specifications that don't match what their usual suppliers carry.

The WhatsApp-first communication model that ibaadu supports reflects how procurement actually operates in the Gulf. Email-based tender processes are standard for formal procurement, but the initial supplier qualification conversation — "do you carry this, can you deliver to this site, what's your lead time" — happens on WhatsApp in this market. A platform that connects you to a regional supplier with direct WhatsApp access removes the friction that kills momentum in time-sensitive procurement situations.

If your procurement team is sourcing construction equipment, materials, or industrial goods for GCC projects and you're not actively building your regional supplier network, you're carrying a risk that's going to materialise when your next delivery deadline gets tight. The market has the supply. The gap is visibility — knowing who has what, where, and when they can deliver it.

Source verified construction suppliers across the GCC

ibaadu connects Gulf construction buyers with regional vendors of equipment, materials, and industrial goods — with direct WhatsApp access to qualified suppliers.

Browse Suppliers on ibaadu →Frequently Asked Questions

What is the size of the GCC construction market in 2026?

The GCC construction market is valued at USD 182.34 billion in 2026 and forecast to reach USD 222.38 billion by 2031 at a 4.05% CAGR, driven by Saudi Vision 2030, UAE's 2040 Urban Master Plan, and infrastructure programmes across Qatar, Oman, Kuwait, and Bahrain.

Which country dominates GCC construction procurement?

Saudi Arabia leads with 45.62% of total GCC construction activity and the fastest CAGR at 5.36% through 2031, underpinned by giga-projects including NEOM, Diriyah, and the Red Sea Project. The UAE is the second-largest market, with a more mature private sector procurement ecosystem.

How are Hormuz Strait disruptions affecting GCC construction supply chains?

Procurement teams sourcing via Hormuz-routed shipping are adding secondary supplier sources from India, Southeast Asia, and East Africa. Port delays now average 12–18 days longer than 2024 baselines, and smart buyers are pre-positioning critical inventory 6–8 weeks ahead to protect project schedules.

Where can I find verified construction equipment suppliers in the Gulf?

ibaadu.com is a B2B trade marketplace focused exclusively on the Middle East, connecting buyers across the GCC with verified regional suppliers of construction equipment, materials, and industrial goods. Browse by category, country, and product specification at ibaadu.com.

Bottom Line for GCC Procurement Teams

The $182 billion GCC construction market isn't slowing down — and neither is the pressure on procurement teams tasked with delivering it. The combination of Vision 2030's sustained investment pipeline, UAE infrastructure expansion, and the supply chain stress caused by Hormuz disruptions has created a sourcing environment where the buyers with the best regional supplier networks consistently outperform those running on outdated vendor lists.

The equipment and materials are in the market. The challenge is visibility — knowing which suppliers have available capacity, qualifying them against regional compliance requirements, and moving fast enough to protect project milestones. Procurement teams that invest in building their regional supplier network now, before the 2027 project wave intensifies further, will have a structural advantage that's very hard to replicate under deadline pressure.

Start building that network today. ibaadu.com connects construction buyers across the Gulf with verified regional suppliers — with direct WhatsApp access for fast-moving procurement decisions.

Ready to source smarter across the GCC?

Visit ibaadu.com →