In this article

The Gulf has quietly become the world's most active region for AI data center construction. In the first five months of 2026 alone, more than US$20 billion in fresh capital has been committed to hyperscale campuses across the UAE and Saudi Arabia, anchored by the US-UAE Stargate cluster in Abu Dhabi, AWS's $5 billion AI Zone with HUMAIN in Riyadh, and a $10 billion Google-PIF partnership announced earlier this year. For B2B buyers in the region, this is no longer a story about technology trends — it is a procurement story with real, near-term consequences for steel, copper, switchgear, cooling equipment and chip allocation. The pace at which contracts are being tendered and awarded has already outstripped the absorption capacity of several specialist supplier categories, and that pressure is now flowing back into pricing and lead times across the wider Gulf construction supply chain.

This Trade Insights briefing breaks down where the money is being spent, what categories of suppliers stand to win, and the bottlenecks that GCC importers and contractors should plan around in the next 18 months. Whether you sell electrical components, HVAC systems, civil works packages or specialist services, the data-center wave is shifting how Gulf procurement teams are sequencing tenders, negotiating with vendors and managing currency and lead-time risk. We also look at the practical implications for SMEs that are not direct hyperscaler suppliers but feed second- and third-tier into the build-out — from local fabricators of stainless ductwork to specialist installers, logistics providers and certified calibration services. The opportunity is broad, but only for vendors who position early and credibly.

The $20 Billion GCC AI Infrastructure Build-Out

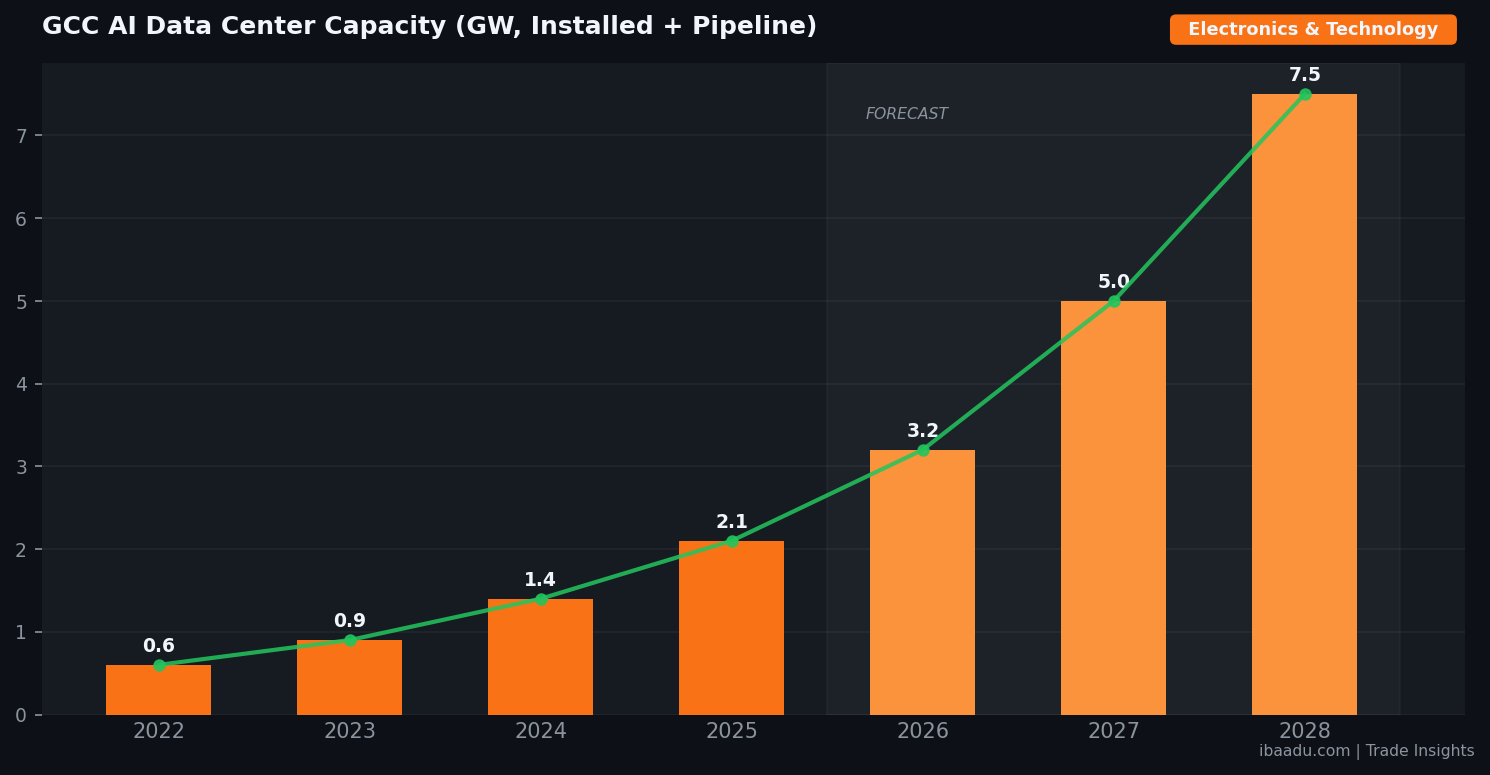

Saudi Arabia and the UAE together now host the largest concentration of announced AI data-center capacity outside the United States. HUMAIN, the Kingdom's state-backed AI champion, plans to bring 100 MW of capacity online across Riyadh and Dammam in Q2 2026, with a stated roadmap to add 1.9 GW by 2030. In the UAE, the Stargate campus in Abu Dhabi — developed jointly by G42, Oracle, NVIDIA, Cisco and SoftBank — targets a 1 GW first cluster, with phase one of 200 MW expected to go live within this calendar year. Microsoft has separately signalled US$7.9 billion in additional UAE investment through 2029, nearly quadrupling its local compute footprint. Regional analysts put the total committed spend across both markets at well over US$50 billion when long-dated phases are included, with roughly US$20–22 billion actively in construction or procurement today. Beyond the headline campuses, second-wave sites are being announced almost monthly: edge facilities in Sharjah, Madinah and Jeddah, sovereign AI zones in Oman, and a joint Bahrain-Kuwait commercial cloud corridor under early-stage discussion. Egypt and Jordan are also entering the conversation as cost-competitive locations for training workloads that do not require ultra-low-latency access to Gulf users. For Gulf manufacturers and distributors, the implication is clear: demand for data-center-grade equipment will not be concentrated in two cities but spread across the wider Arab world.

Inside Procurement: What Hyperscale Sites Are Buying

Behind every megawatt of AI capacity is a deep procurement stack. Hyperscale operators typically allocate around 40 percent of build cost to mechanical and electrical equipment — uninterruptible power supplies, switchgear, transformers, generators, busways, precision air-conditioning, chilled-water plants and liquid-cooling skids. A further 20–25 percent is structural and civil: rebar, post-tensioned concrete, raised-access flooring, fire-rated partitions, and security-graded perimeter works. Cabling, fibre optics, low-voltage systems and BMS controls add another meaningful share. For GCC suppliers, this means opportunities are concentrated in three buckets: (1) heavy electrical equipment, where global lead times for transformers above 100 MVA have stretched past 80 weeks; (2) liquid-cooling components for GPU racks, an area where regional fabrication capacity is still nascent; and (3) civil and MEP sub-contracting at scale, which favours contractors with credible track records on Aramco, ADNOC or Saudi giga-project sites. A growing fourth category is rapid-deploy modular infrastructure: prefabricated power and cooling pods shipped from factories in Asia or Europe and integrated on-site in weeks rather than months. Several Gulf operators have already standardised on modular designs to compress the time-to-revenue for new AI training capacity, and this in turn has opened tenders for local logistics, lifting, and commissioning services that did not exist at this scale two years ago. For procurement leaders, the lesson is to map the full bill of materials before the first foundation is poured.

Source Verified B2B Suppliers on ibaadu

Connect directly with Electronics & Technology suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Power, Cooling and the Supply-Chain Squeeze

The single biggest risk to the GCC AI build-out is not capital — it is power and supply chain. A 1 GW campus consumes electricity equivalent to a small city, and transmission upgrades are now on the critical path for multiple sites. Saudi Arabia is fast-tracking 380 kV interconnections to NEOM and the Eastern Province, while DEWA and TAQA are accelerating substation construction in Abu Dhabi to feed the Stargate footprint. Cooling is the second pressure point: ambient temperatures in the Gulf push operators toward closed-loop, direct-to-chip liquid cooling rather than traditional air systems. That, in turn, drives demand for stainless-steel piping, coolant distribution units, and water-treatment chemistry — categories where Asian and European suppliers currently dominate. Tariff posture remains favourable: the UAE and Saudi Arabia have kept import duties on most data-center equipment at or near zero, and recent clarifications on US export licensing of advanced GPUs have reopened a steady chip pipeline into Gulf operators with approved end-use agreements. On the workforce side, the shortage of certified electrical commissioning engineers and high-voltage technicians is forcing operators to fly in specialist teams from Europe and South Asia, adding 8 to 12 percent to project costs in some cases. Local training initiatives in both Saudi Arabia and the UAE are beginning to close that gap, but supply-chain leaders should plan for elevated labour costs and competition for qualified MEP subcontractors well into 2027.

What Buyers and Suppliers Should Do in 2026

For procurement teams on the buyer side, the practical advice is to lock long-lead items now. Operators tendering second-half 2026 builds should already have transformer and switchgear orders placed, and should be qualifying at least two cooling-equipment vendors in parallel. Pre-negotiated frame agreements with EPC partners are increasingly common, and large buyers are bundling civil, MEP and IT-fit-out into a single design-build package to compress schedule. For suppliers and exporters looking to enter Gulf data-center supply chains, three things matter: certification (operators want IEC, UL and where relevant TIA-942 compliance), a credible local service footprint or partner, and demonstrated reference projects. Listing on a verified B2B platform shortens the discovery phase: ibaadu lets manufacturers and distributors publish capability profiles that procurement teams in Abu Dhabi, Riyadh, Doha and Muscat can screen directly, without paying intermediary commissions. With the AI build-out only in its first year, vendors who establish reference accounts in 2026 will be best placed to participate in the much larger 2027–2028 expansion phase. Smaller suppliers should consider forming consortia to bid on packages that would be too large individually, and should invest early in compliance documentation and after-sales service capability — two areas where regional operators consistently flag dissatisfaction with new entrants. The window to become a default-tier vendor in the Gulf AI ecosystem is open now, and it will close as soon as the operators settle on their preferred panels.

Frequently Asked Questions

How much is being invested in AI data centers across the GCC in 2026?

Approximately US$20-22 billion is actively in procurement or construction in 2026 across the UAE and Saudi Arabia, with total announced commitments through 2030 exceeding US$50 billion across projects such as Stargate UAE, HUMAIN, the AWS AI Zone and Microsoft's UAE expansion.

What product categories see the biggest procurement uplift?

Medium- and high-voltage transformers, switchgear, UPS systems, precision air conditioning and liquid-cooling equipment lead demand, followed by structural steel, post-tensioned concrete, raised-access flooring, fibre optics and low-voltage controls. Long-lead electrical items are the most supply-constrained.

Are import duties on data-center equipment a barrier in the UAE or Saudi Arabia?

Generally no. Both the UAE and Saudi Arabia maintain low or zero customs duties on most ICT and electrical equipment used in licensed data-center projects. Strategic or end-use restrictions apply to certain advanced semiconductors and require US export-license alignment.

How can a supplier get qualified for these projects?

Operators typically require IEC, UL or TIA-942 compliance where applicable, a local service presence or accredited partner, and verifiable reference projects. Listing on verified B2B platforms such as ibaadu accelerates discovery by procurement teams across the GCC and removes intermediary commissions from the sourcing process.

Conclusion

The GCC's AI data center boom is moving from announcement to steel-in-the-ground at unprecedented speed. Combined committed capacity across the UAE and Saudi Arabia is on track to roughly triple by end-2027, with knock-on demand for everything from medium-voltage switchgear to specialty coolants and precision fabrication. Buyers who plan procurement on an 18-month horizon and suppliers who position now will find the next two years the most opportunity-rich window the Gulf tech-infrastructure market has ever seen. For both sides, the value of transparent, direct B2B sourcing has rarely been higher, and the operators who execute fastest will set the procurement standards that the rest of the market follows.