In this article

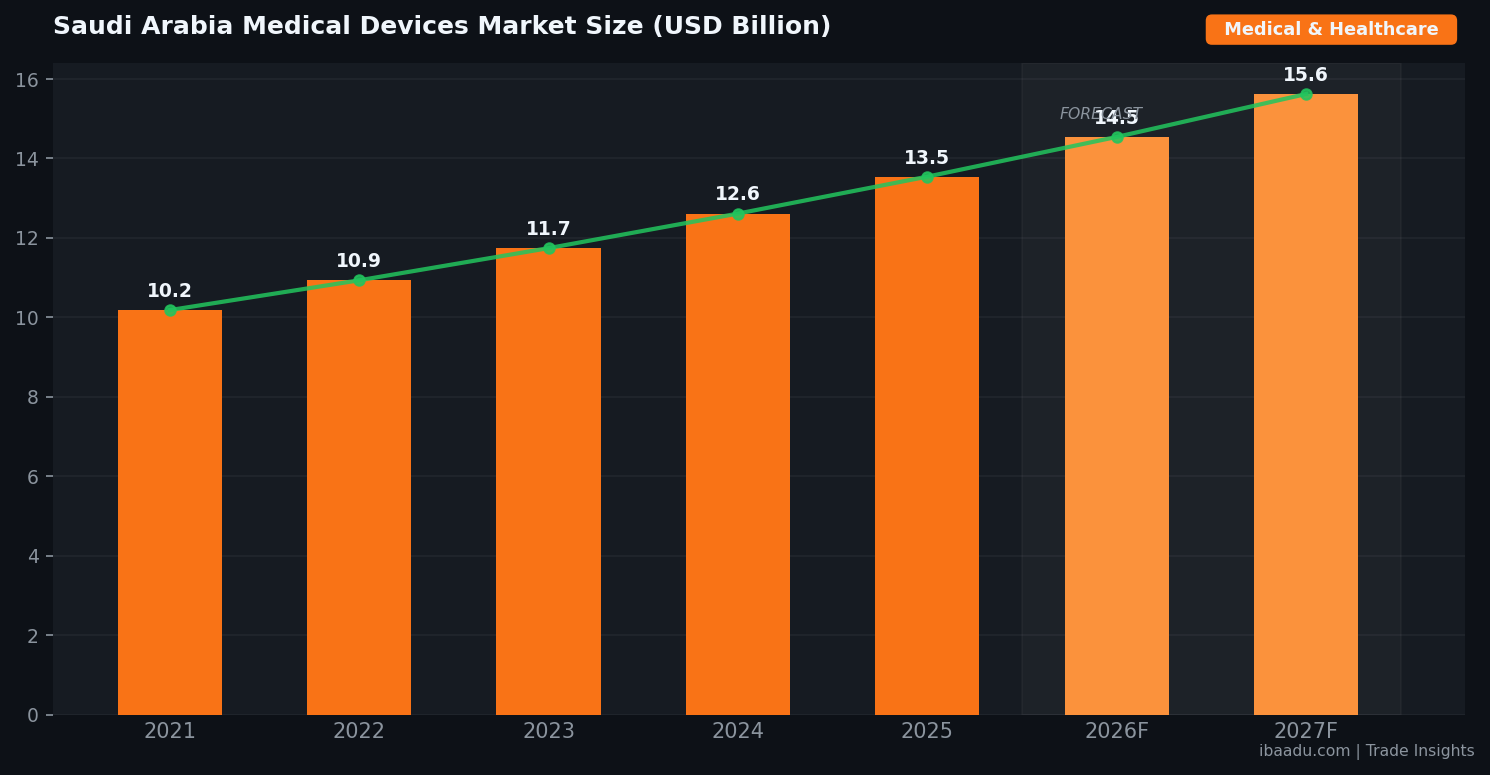

The GCC medical devices market is entering a period of sustained, policy-driven growth that is reshaping B2B procurement dynamics across the Gulf. Saudi Arabia's medical devices sector, valued at approximately USD 13.54 billion in 2025, is on a trajectory to reach USD 25.74 billion by 2034, driven by a compound annual growth rate of 7.4 percent. At the same time, the broader MENA medical device market is forecast to hit USD 34.95 billion by 2032, with Saudi Arabia and the UAE together accounting for roughly 92 percent of GCC healthcare transactions.

For B2B buyers, procurement managers, and suppliers operating across the Gulf, 2026 marks an inflection point. New localisation rules, tightening regulatory frameworks, and a decisive shift toward single-use, infection-control-oriented products are changing who wins contracts and how supply chains must be structured. This report examines the forces reshaping GCC medical device procurement and the practical strategies that will distinguish winning suppliers and buyers in the year ahead.

GCC Healthcare Infrastructure: The Demand Engine Behind Device Growth

Two overarching national agendas are doing the heavy lifting behind GCC medical device demand. Saudi Arabia's Vision 2030 has earmarked substantial capital for healthcare modernisation, with new hospitals, diagnostic centres, and specialty clinics under construction across the Kingdom. The UAE's "We the UAE 2031" strategy complements this with a push toward smart hospitals equipped with AI-integrated imaging, robotic surgery systems, and connected patient monitoring infrastructure. Together, these programmes represent multi-decade demand pipelines for equipment suppliers and consumable distributors.

On the institutional side, the Gulf Health Council manages a consolidated procurement mechanism that allows member states to aggregate demand and negotiate bulk pricing across GCC member countries. This arrangement benefits suppliers who can commit to volume delivery schedules, but it also raises the bar on quality certification and after-sales service. Hospitals in Qatar, Oman, Kuwait, and Bahrain increasingly reference GHC framework pricing when benchmarking independent procurement, which means that competitive pricing across the wider GCC is now effectively interconnected.

Population demographics are adding further pressure to capacity. The UAE's expatriate-heavy population, combined with growing rates of non-communicable diseases — particularly diabetes and cardiovascular conditions — across all GCC states, is generating consistent demand for diagnostic imaging, cardiac monitoring, and chronic disease management equipment. Saudi Arabia's youthful population profile is simultaneously expanding demand for maternal and neonatal care equipment. Procurement managers at both public and private hospital networks are responding by diversifying supplier bases and extending contract durations, shifting from spot purchasing to framework agreements that guarantee supply security over 24 to 36-month cycles.

Private healthcare investment is compounding the public sector's procurement activity. Several GCC-based hospital groups have announced capacity expansions in 2025 and 2026, and international operators entering the market under concession or joint-venture arrangements bring their own global supply relationships — creating opportunities for established international suppliers while also raising competitive pressure on regional distributors.

Key Product Categories and Sourcing Priorities for 2026

Six product categories have emerged as the dominant demand drivers in GCC procurement cycles for 2026. Diagnostic imaging equipment — including MRI, CT, and ultrasound systems — tops the list, as new hospital facilities require full fit-outs and existing facilities undertake technology refresh cycles to upgrade analogue systems to digital and AI-enhanced platforms. Procurement teams are increasingly specifying AI-assisted image interpretation capabilities as a standard requirement rather than an optional add-on, which is raising the average contract value and filtering out lower-specification suppliers.

Patient monitoring systems represent the second major category, driven by intensive care expansion and step-down ward upgrades. Wireless and IoT-enabled monitoring platforms are preferred in new builds, while retrofit projects in established facilities continue to demand bedside units with integration capability for existing hospital information systems. Suppliers able to offer full lifecycle support — installation, training, preventive maintenance, and software updates — command a significant pricing premium and win preferred vendor status in long-term agreements.

Surgical instruments and consumables, laboratory equipment, in-vitro diagnostics, and telemedicine platforms complete the priority list. The consumables sub-sector is undergoing a structural shift as GCC hospitals accelerate the replacement of reusable items with single-use equivalents under stricter hospital-acquired infection prevention protocols. This shift is not marginal: procurement managers at major Saudi hospital networks report that budgets for single-use surgical consumables have increased by 15 to 25 percent year-on-year as infection control policies are formalised and audited. Suppliers who can deliver CE-certified consumables at volume with consistent batch quality are winning multi-year framework agreements ahead of competitors offering lower per-unit pricing but inconsistent supply.

Telemedicine infrastructure is the fastest-growing sub-category by percentage growth, albeit from a lower base. UAE government mandates for digital health records and remote consultation capabilities at licensed facilities have created a new procurement stream for telehealth platforms, remote monitoring devices, and secure data transmission equipment. Oman and Bahrain are following with similar digital health roadmaps, opening adjacent procurement opportunities for suppliers already established in the UAE market.

Source Verified B2B Suppliers on ibaadu

Connect directly with Medical & Healthcare suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Regulatory Compliance and Localisation Requirements

Regulatory compliance in GCC medical device procurement has grown considerably more complex over the past two years, and 2026 represents the first full cycle in which several new frameworks are fully enforced. In Saudi Arabia, the Saudi Food and Drug Authority (SFDA) has tightened post-market surveillance requirements, mandating that registered suppliers submit adverse event reports within defined timelines and maintain in-Kingdom technical service capability. Foreign manufacturers without a local registered agent face delays in licence renewal that can effectively lock them out of NUPCO tenders for months at a time.

NUPCO — the National Unified Procurement Company — remains the central gateway for public hospital procurement in Saudi Arabia, managing framework agreements that cover thousands of product lines across all 13 regions. The most significant procurement policy shift of 2026 is NUPCO's active prioritisation of local alternatives: the organisation has begun rejecting bids from foreign suppliers when a domestically manufactured or locally assembled equivalent product is available and certified. This policy is backed by Saudi Arabia's Local Content and Government Procurement Authority (LCGPA) and the "Made in Saudi" programme, which provides accreditation and marketing support to qualifying manufacturers.

For international suppliers, the practical response is clear: establishing local assembly partnerships, technology transfer agreements with Saudi manufacturers, or joint ventures with SFDA-licensed local entities is moving from a competitive advantage to a compliance necessity. Several European and East Asian medical device companies have entered into manufacturing partnerships with Saudi firms in 2025 and early 2026, explicitly to protect their NUPCO market access as localisation requirements tighten.

In the UAE, the regulatory picture is somewhat more open, with MOHAP and emirate-level health authorities maintaining CE marking and FDA 510(k) clearance as the primary certification benchmarks. However, the UAE's Operation 300bn industrial strategy rewards suppliers who establish local assembly or manufacturing through preferential treatment in public procurement evaluation scoring. Abu Dhabi's KIZAD free zone has attracted several medical device assembly operations, and Dubai's HealthPoint cluster continues to draw regional headquarters relocations from companies seeking to consolidate GCC regulatory registrations. For B2B buyers in the UAE, this means a growing pool of locally based, GCC-registered suppliers who can offer shorter lead times and greater flexibility on minimum order quantities than import-only competitors.

B2B Procurement Strategies: Winning Supplier and Buyer Approaches

The procurement landscape of 2026 rewards suppliers and buyers who take a structured, relationship-oriented approach over transactional spot-buying. For suppliers, the single most important strategic move is achieving multi-country regulatory registration in parallel rather than sequentially. Registering with SFDA, MOHAP, and the Qatar National Health Authority concurrently — even if market entry is prioritised in one country — allows suppliers to respond rapidly when a framework tender covers multiple GCC jurisdictions, which is increasingly common as the Gulf Health Council's consolidated procurement scope expands.

Buyers, for their part, are moving toward consolidated supplier panels rather than managing large numbers of approved vendors. The operational overhead of managing SFDA audits, CE certificate renewals, and ISO 13485 quality management reviews for dozens of suppliers is driving procurement teams to reduce their approved vendor lists and deepen relationships with a smaller number of strategically important partners. This consolidation benefits suppliers who invest in account management, technical support capability, and proactive communication on product updates and regulatory changes — and disadvantages those who compete on price alone.

Financing and payment terms have emerged as a significant differentiator in GCC medical device procurement. Public hospital procurement cycles often involve extended payment timelines, and suppliers who can accommodate 60 to 90-day payment terms without punitive pricing adjustments are viewed more favourably in bid evaluation. Several regional banks and trade finance providers have introduced supply chain finance programmes specifically targeting GCC healthcare procurement, allowing suppliers to offer extended terms to buyers while receiving early payment from the financing institution. B2B buyers who have not yet explored these programmes may find that they provide leverage to negotiate better pricing from suppliers who value the payment certainty.

Digital procurement platforms are increasingly embedded in GCC hospital procurement workflows. Systems that integrate SFDA and MOHAP registration status, provide real-time inventory visibility, and support electronic purchase order and invoice processing are becoming prerequisites for preferred supplier status at major hospital groups. Suppliers investing in EDI integration and API connectivity with hospital procurement systems are building switching costs that protect long-term contract relationships, while buyers who standardise their procurement technology gain better data for demand forecasting and compliance reporting.

Frequently Asked Questions

How large is the GCC medical devices market in 2026?

The GCC medical consumables segment alone is projected at USD 495 million in 2026, while Saudi Arabia's broader medical devices market is estimated at approximately USD 14.5 billion for the year. The wider MENA medical device market is forecast to reach USD 34.95 billion by 2032.

What certifications do medical device suppliers need to sell in the UAE and Saudi Arabia?

Suppliers must hold CE marking (EU MDR) or FDA 510(k) clearance as a baseline. In Saudi Arabia, registration with the Saudi Food and Drug Authority (SFDA) is mandatory. In the UAE, approval from the Ministry of Health and Prevention (MOHAP) or the relevant emirate health authority is required before commercial supply.

What is NUPCO and why does it matter for B2B medical procurement in Saudi Arabia?

NUPCO (National Unified Procurement Company) is Saudi Arabia's centralised purchasing authority for government hospitals. It manages framework agreements covering thousands of product lines. Since 2026, NUPCO has actively prioritised local or locally assembled products under LCGPA localisation rules, meaning international suppliers must partner with local agents or establish in-country assembly to remain competitive.

Which medical equipment categories offer the strongest B2B growth opportunities in the GCC in 2026?

The six categories showing the strongest demand trajectory are: diagnostic imaging equipment, patient monitoring systems, surgical instruments and consumables, laboratory equipment, in-vitro diagnostics, and telemedicine platforms. Infection-control consumables and single-use surgical items are also growing rapidly as hospitals comply with stricter HAI prevention protocols.

Conclusion

The GCC medical devices market in 2026 is defined by two simultaneous forces: accelerating demand driven by Vision 2030, We the UAE 2031, and expanding private healthcare investment; and tightening supply-side requirements as localisation mandates, stricter regulatory enforcement, and consolidating procurement frameworks raise the bar for market participation. Suppliers who have built multi-country regulatory registrations, established local partnerships or assembly capability, and invested in digital procurement integration are positioned to capture disproportionate share of a rapidly growing market. Buyers who consolidate their approved vendor panels, leverage supply chain finance to improve payment terms, and deepen technical partnerships with strategic suppliers will find they are better insulated from supply disruptions and better positioned for the contract renewals that will define procurement relationships through the decade. ibaadu's B2B platform connects verified medical and healthcare suppliers with procurement teams across the GCC — enabling the direct, transparent partnerships that this market increasingly demands.