In this article

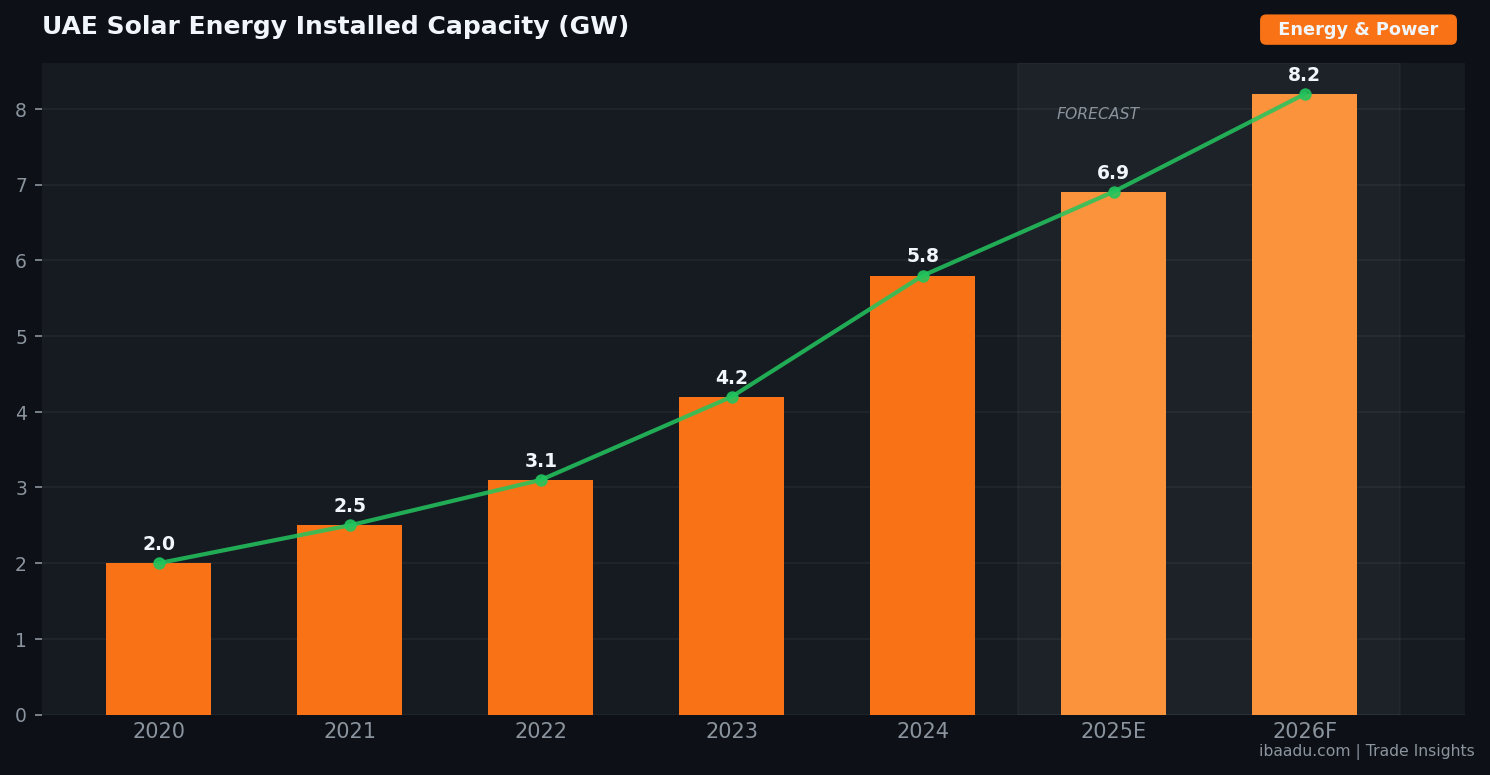

The UAE's solar energy sector has undergone a remarkable transformation over the past five years, evolving from a niche government-led initiative into a mainstream infrastructure asset class attracting billions of dollars in annual B2B procurement spend. With installed solar capacity projected to reach 8.2 GW by the end of 2026 — up from just 2.0 GW in 2020 — the supply chain behind that expansion is generating substantial commercial opportunities for buyers and sellers across the Gulf Cooperation Council.

For procurement managers, project developers, and corporate energy buyers, this moment requires a clear-eyed understanding of the market: where to source modules and balance-of-system components, how to structure EPC contracts, which specifications regulators now demand, and how to manage a supply chain that remains partly exposed to global logistics volatility. This guide, drawn from ibaadu's Trade Insights research, provides a practical framework for GCC buyers looking to capitalise on the solar procurement boom in 2026.

The Scale of the UAE Solar Opportunity in 2026

The numbers underpinning the UAE solar market are striking even by Gulf standards. The UAE's updated National Energy Strategy commits the country to tripling its renewable capacity to 14 GW by 2030, raising the share of clean energy in the national mix to 30% by 2031, and achieving full carbon neutrality by 2050. To meet these targets, the UAE needs to add roughly 1–1.5 GW of new solar capacity every year for the remainder of this decade — a pipeline that translates directly into sustained procurement demand for panels, inverters, mounting systems, cables, monitoring equipment, and EPC services.

Dubai Electricity and Water Authority (DEWA) remains the most prominent single buyer in the market, with its Mohammed bin Rashid Al Maktoum Solar Park now representing one of the world's largest single-site solar installations. The park is scheduled to reach 5 GW of total capacity by 2030, with multiple phases currently under construction or in procurement. Abu Dhabi's TAQA and Masdar are running parallel programmes, having recently broken ground on projects that will collectively add more than 2 GW of utility-scale capacity in the emirate by 2027. In the Northern Emirates, Sharjah Electricity and Water Authority (SEWA) and Ras Al Khaimah's RAK Energy are accelerating their own distributed solar programmes.

Beyond the utility sector, the corporate power purchase agreement (PPA) market has emerged as a major source of incremental demand. Free zone operators, logistics park developers, and large industrial manufacturers are increasingly procuring behind-the-meter solar systems in the 1–50 MWp range to hedge against tariff increases and satisfy ESG reporting requirements. Jebel Ali Free Zone (JAFZA), Dubai Industrial City, and Abu Dhabi's Khalifa Industrial Zone (KIZAD) have all rolled out solar incentive frameworks over the past 18 months, creating a new tier of mid-market B2B procurement that sits between small commercial rooftop systems and mega utility projects.

What B2B Buyers Need to Know Before Sourcing Solar Equipment

Sourcing solar equipment for GCC projects in 2026 requires buyers to navigate a more complex technical and regulatory landscape than existed even two years ago. DEWA and the Abu Dhabi Department of Energy have both updated their approved vendor lists (AVLs) and technical specifications in response to rapid product evolution, and procurement teams that rely on outdated standards risk specification mismatches, import delays, or warranty voidance.

On the module side, the industry has largely converged on bifacial monocrystalline silicon technology — specifically PERC and next-generation TOPCon architectures — for utility and commercial-scale projects. Leading manufacturers supplying the UAE market include Tier 1 Chinese producers (LONGi, JA Solar, Jinko, Trina) alongside European and Southeast Asian suppliers. Buyers should prioritise modules rated at 580 Wp and above, as higher-wattage panels reduce balance-of-system costs by minimising the number of strings and structural mounting points per megawatt. IEC 61215 and IEC 61730 certifications are non-negotiable; DEWA additionally requires modules to appear on its own AVL, which is updated quarterly.

Inverter procurement deserves equal attention. String inverters dominate the commercial segment (systems below 5 MWp), while central inverters remain prevalent in utility installations. Leading inverter brands active in the UAE include Huawei, SMA, FIMER, and ABB Power Grids. For projects subject to DEWA's Smart Grid compliance requirements, buyers must ensure inverters are certified to IEC 62116 for anti-islanding protection and carry cybersecurity certifications increasingly required under UAE's national cybersecurity framework. Lead times for inverters have stabilised in 2026 after the 2022–2024 logistics disruption period, but buyers are still advised to lock in supply agreements 16–20 weeks before the required on-site delivery date.

Source Verified B2B Suppliers on ibaadu

Connect directly with Energy & Power suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Navigating EPC Contract Procurement in the GCC

For buyers developing projects above 500 kWp, the engineering, procurement, and construction (EPC) contract is typically the single largest line item in a solar project's budget, often representing 60–75% of total installed cost. Selecting and contracting the right EPC partner is therefore among the most consequential procurement decisions a GCC project developer or corporate energy buyer will make.

The EPC landscape in the UAE has matured considerably since 2020. The market now features a defined hierarchy: at the top sit large-scale international EPC contractors (ACWA Power, Engie, Masdar's development arm, and major Indian EPCs including Sterling & Wilson and Tata Power Solar) who typically target projects above 50 MWp. The mid-market — projects in the 1–50 MWp range — is served by a growing cohort of UAE-registered EPC firms with strong regional track records, including several companies now certified under Abu Dhabi's In-Country Value (ICV) programme. Below 1 MWp, the market is highly fragmented, with dozens of local installation and integration companies competing primarily on price.

Buyers procuring EPC services should structure their tender documents to capture the full scope of the contractor's obligations: civil works (pile or ballast foundations, cabling trenches), electrical works (LV and MV cabling, transformer, switchgear), SCADA and monitoring systems, grid connection coordination, testing and commissioning, and the performance guarantee mechanism. A well-structured performance guarantee — typically a minimum annual energy production figure calculated using PVGIS solar resource data — is essential for protecting the buyer's investment return, particularly for PPA-financed projects where revenue is directly linked to system output. Buyers should negotiate performance guarantees at 90% of the P90 production estimate and require performance bonds of 10–15% of the contract value to ensure contractor accountability.

The request for proposal (RFP) process for GCC solar EPC contracts typically runs 8–14 weeks for commercial projects, including pre-qualification, technical evaluation, commercial negotiation, and contract execution. Utility-scale projects above 50 MWp can take 12–18 months from RFP issuance to financial close, partly because multi-tier bid evaluation processes mandated by government procuring entities include mandatory site visits, reference project verification, and legal review of the power purchase agreement or connection agreement with the utility.

Price Trends, Lead Times, and Supply Chain Risks in 2026

After three years of significant price volatility driven by polysilicon shortages, shipping disruptions, and currency fluctuations, the global solar supply chain has entered a period of relative stabilisation in 2026 — though new risks have emerged that GCC procurement teams must track closely.

Module prices have declined substantially from their 2022 peak of approximately USD 0.28–0.32 per watt (Wp) for Tier 1 bifacial modules, and now sit in the USD 0.13–0.17/Wp range for large-volume orders placed directly with manufacturers. This price compression reflects the massive capacity expansion by Chinese manufacturers, who now account for over 80% of global module production. For UAE buyers, this creates a price opportunity but also concentration risk: any disruption to Chinese production or export logistics — whether from geopolitical events, new tariff regimes, or extreme weather — can cause rapid price spikes and supply shortfalls. Buyers with projects commencing construction in Q3 or Q4 2026 should consider hedging by placing firm orders with 20–30% deposit at least 6 months in advance.

Logistics costs between key Asian manufacturing hubs and GCC ports have normalised after the 2021–2023 container shipping crisis, with Jebel Ali Port handling a growing share of UAE solar imports directly. Customs clearance for solar panels, inverters, and mounting systems in the UAE typically takes 5–10 working days under standard import procedures, though buyers working under DEWA or ADNOC contracts may be eligible for expedited customs processing under approved supplier frameworks. It is worth noting that UAE import duties on solar modules are currently zero under the GCC Common External Tariff (CET), which meaningfully reduces total landed cost compared to markets that have introduced anti-dumping duties on Chinese panels.

Battery energy storage system (BESS) procurement is the fastest-growing adjacent market. Developers adding storage to solar projects are seeing lithium iron phosphate (LFP) battery prices at approximately USD 90–110/kWh at the module level in 2026, down from over USD 200/kWh in 2022. Buyers who intend to add storage should plan procurement timelines independently of the solar EPC, as BESS lead times remain longer than module supply chains — typically 20–28 weeks from order to delivery for large utility-scale systems.

Frequently Asked Questions

What solar panel specifications are most commonly required in UAE utility-scale projects?

UAE utility-scale projects typically specify bifacial monocrystalline PERC or TOPCon modules rated at 580–670 Wp, with a degradation rate below 0.45% per year and a 25–30 year linear power output warranty. Buyers should also confirm IEC 61215 and IEC 61730 certification, as well as compliance with DEWA or the relevant emirate authority's approved vendor list (AVL).

How long does EPC procurement typically take for a commercial solar project in the UAE?

For commercial rooftop systems (100 kWp–1 MWp), the EPC procurement cycle typically runs 8–14 weeks from tender issuance to contract award. Utility-scale projects above 50 MWp can take 6–18 months due to technical evaluation, reference site visits, and multi-round bidding. Engaging pre-qualified EPC contractors early — ideally 3–6 months before the project financial close — significantly compresses timelines.

Are there local content requirements for solar projects in the UAE?

Yes. DEWA and Abu Dhabi's ADNOC-aligned programmes incorporate in-country value (ICV) scoring into procurement evaluation. Suppliers and EPC contractors are assessed on the share of UAE-manufactured or assembled components, local workforce employment, and technology transfer commitments. Buyers should request ICV certificates and factor ICV scores into bid evaluation weightings alongside price and technical merit.

What financing structures are typically used for B2B solar procurement in the GCC?

GCC B2B buyers most commonly use one of three structures: (1) direct CAPEX purchase, which delivers the highest long-term ROI; (2) a Power Purchase Agreement (PPA) with an independent power producer, which eliminates upfront cost; or (3) a lease or equipment finance arrangement through a GCC bank or specialised green finance provider. UAE banks including Emirates NBD and Abu Dhabi Islamic Bank now offer dedicated solar financing products with tenors up to 15 years at competitive rates tied to project performance guarantees.

Conclusion

The UAE's solar procurement market in 2026 represents one of the most dynamic B2B opportunities in the Middle East energy sector. With installed capacity set to more than double by 2030, procurement teams across the GCC have a multi-year window to build supply chain relationships, develop in-house technical expertise, and position their organisations to benefit from one of the region's most capital-intensive infrastructure programmes. The key to capturing value lies in preparation: understanding current module and inverter specifications, structuring EPC tenders rigorously, monitoring supply chain price signals, and leveraging platforms like ibaadu to identify and qualify verified suppliers before competition for preferred vendors intensifies. Buyers who act now — building supplier panels, standardising procurement frameworks, and engaging with the EPC market proactively — will secure better pricing, shorter lead times, and stronger performance guarantees than those who wait until construction pressure forces reactive purchasing decisions.