In this article

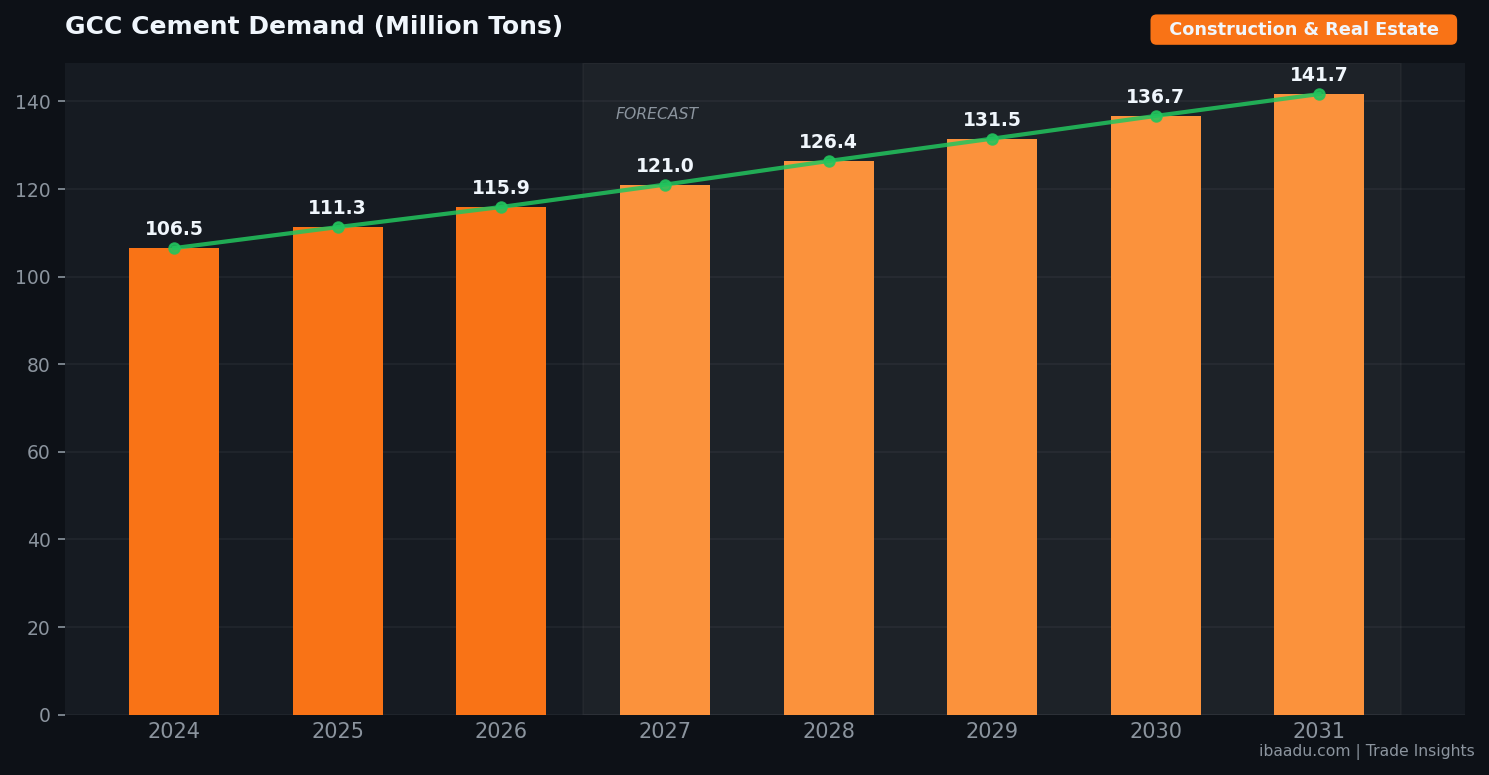

The Gulf Cooperation Council cement market crossed a meaningful threshold in 2026: USD 9.1 billion in annual value, roughly 115.86 million tons of consumption, and a forecast trajectory that places it firmly at 141.7 million tons and beyond USD 15 billion within the next decade. For B2B procurement teams serving construction, real estate and infrastructure clients across the Middle East, that single statistic reframes how cement should be sourced, contracted and stockpiled for the rest of the decade.

This Trade Insights report unpacks the demand surge driving GCC cement volumes, the country-level pipelines absorbing the tonnage, the procurement frictions creeping into pricing, and the practical positioning steps buyers can take in 2026 to lock in supply security without paying intermediary premiums. The data tells a clear story: megaproject ambition is finally turning into committed cement tonnage on the ground.

The $9.1 Billion Number: What 2026 Demand Really Looks Like

The headline figure, USD 9.1 billion in GCC cement market value for 2026, looks deceptively orderly. Underneath, it is the result of three converging forces: government-led megaproject delivery accelerating after years of design and tender work, a private real estate cycle that has refused to cool in Dubai and Abu Dhabi, and substitution of imported cement and clinker by domestic GCC producers chasing capacity utilisation. Together those forces push 2026 consumption to roughly 115.86 million tons, up from about 111.27 million tons in 2025.

What makes the 2026 demand pattern unusual is its evenness. Historically, GCC cement consumption has been highly cyclical, tied to oil revenue and individual flagship projects. In 2026, demand is broad-based: Saudi Arabia, the UAE, Qatar and Oman are each simultaneously executing multi-year infrastructure pipelines, with Bahrain and Kuwait supplying steady but smaller volumes. The result is a 4.12 percent CAGR through 2031 and a 5.7 percent value CAGR through 2036, both well above the global cement industry average of roughly 2 to 3 percent.

For procurement teams, the practical implication is that the traditional GCC cement buying playbook, opportunistic spot purchasing during oil price downturns, no longer works as well. Capacity that historically sat idle is now spoken for, and producers are increasingly comfortable holding price during demand softness because their order books extend twelve to eighteen months forward. Buyers who treat 2026 like 2018 are likely to be surprised by both lead times and pricing rigidity.

Country-by-Country: Where the Cement Tonnage Is Flowing

Saudi Arabia is the centre of gravity. The Kingdom is on track to consume more than 55 million tons of cement in 2026, driven by NEOM and The Line vertical structures finally entering bulk concrete phases, Qiddiya entertainment city, the Red Sea Project hotels and infrastructure, Riyadh Metro line extensions, the Roshn national housing programme and the World Cup 2034 stadium and transport build-out. The Saudi figure alone exceeds the combined consumption of every other GCC state.

The UAE is the second pillar, projected at roughly 28 to 30 million tons in 2026. Dubai 2040 Urban Master Plan keeps the residential and mixed-use pipeline full, while Abu Dhabi infrastructure spending around Saadiyat cultural district, Etihad Rail extensions and industrial cluster expansion at KEZAD adds heavy-haul cement demand. Importantly, UAE cement consumption now includes meaningful volumes for solar farm foundations and data centre slabs, two categories that barely existed five years ago.

Qatar continues to surprise on the upside. Post-World Cup commentary expected a sharp drop, but a USD 70 billion construction market in 2025 and a forecast that nearly doubles by 2034 suggests Qatar will absorb 12 to 14 million tons in 2026. Oman is the fastest-growing per capita consumer, anchored by the Dhofar green hydrogen corridor, Sultan Haitham City and the Duqm Special Economic Zone. Bahrain and Kuwait round out the picture with steady residential and refinery-linked demand.

Source Verified B2B Suppliers on ibaadu

Connect directly with Construction & Real Estate suppliers and manufacturers across the GCC. No middlemen.

Browse Suppliers →Procurement Reality: Pricing, Supply Chains and Carbon Pressure

The pricing picture in 2026 is genuinely mixed, and that mix is where many procurement teams get caught out. On one side, GCC steel prices have risen 15 to 25 percent since recent regional tensions escalated, pulling reinforced concrete project costs up sharply and indirectly tightening cement demand. On the other, domestic GCC cement overcapacity, especially in Saudi Arabia, caps how far producers can push list prices before importers from Oman, Iran or Egypt step back in. Net of those forces, ex-works bagged cement prices in 2026 sit roughly 4 to 7 percent above 2025 levels, with bulk OPC contracts moving in a similar band.

Supply-side pressure is more interesting than price. The widening global demand for low-carbon cement has outpaced slag and fly-ash availability, squeezing GCC producers that depend on those supplementary cementitious materials to meet European-style sustainability specifications increasingly written into Gulf project tenders. Producers that locked multi-year slag offtake from Indian and East Asian steel mills before 2024 now enjoy a meaningful cost advantage, and buyers are starting to ask about embodied carbon clauses in supply contracts as part of standard prequalification.

Shipping and logistics remain the wild card. GCC producers import roughly a quarter of their clinker and most of their gypsum, and Red Sea routing risk has lifted insurance premiums and pushed some shipments around the Cape. Procurement teams that previously treated freight as a stable line item should now build a 3 to 8 percent freight contingency into landed-cost models, especially for projects sitting on the western coast of Saudi Arabia where alternative sourcing is geographically harder.

How B2B Buyers Should Position for 2026–2031

The first move for any serious GCC cement buyer in 2026 is to extend contract horizons. With demand visible eighteen to twenty-four months forward and capacity tighter than the headline overcapacity figure suggests, monthly spot procurement leaves buyers exposed to both lead-time slippage and price drift. Six to twelve month volume contracts with quarterly indexing are becoming the new normal for mid-sized contractors, while large EPC players are increasingly negotiating multi-year cement and ready-mix concrete offtake.

The second move is supplier diversification within country. Concentration risk on a single producer is no longer prudent when delivery schedules are this tight. Most well-run GCC contractors now run a primary supplier at 60 to 70 percent of volume, a secondary at 20 to 30 percent and a spot allocation for surge weeks. Platforms like ibaadu help compress the time required to qualify and onboard secondary suppliers, since the marketplace already standardises documentation, certifications and reference projects in one place.

The third positioning step is embedded carbon strategy. With Saudi Arabia and the UAE both moving toward mandatory whole-life carbon reporting on large projects, buyers who lock in low-carbon cement supply ahead of those rules avoid bidding wars when specifications tighten in 2027 and 2028. Engaging suppliers now about CEM II and CEM III alternatives, calcined clay blends and clinker substitution is a procurement conversation, not just a sustainability one.

Frequently Asked Questions

How large is the GCC cement market in 2026?

The GCC cement market is valued at approximately USD 9.1 billion in 2026, with volumes reaching about 115.86 million tons. Saudi Arabia represents the largest single share, followed by the UAE and Qatar, driven by Vision 2030 megaprojects, NEOM, Red Sea developments and Expo-era UAE infrastructure spending.

Why are GCC cement prices under pressure in 2026?

Cement prices are being pulled in two directions. Megaproject demand, rising clinker costs, supplementary cementitious material shortages and tighter carbon regulation all push prices upward. At the same time, domestic overcapacity in Saudi Arabia and the UAE caps how aggressively producers can raise list prices, leaving buyers in a narrow but volatile pricing band.

Which GCC country has the largest cement procurement pipeline?

Saudi Arabia leads by a wide margin. Between NEOM, The Line, Qiddiya, the Red Sea projects, Riyadh metro extensions and a national housing programme, Saudi Arabia is expected to absorb more than half of all GCC cement consumption through 2030. The UAE follows with sustained demand from Dubai 2040 Urban Master Plan and Abu Dhabi infrastructure.

How can B2B buyers secure stable cement supply on ibaadu?

ibaadu connects verified GCC buyers with cement producers, ready-mix concrete suppliers and aggregate vendors across Saudi Arabia, UAE, Oman, Qatar and Bahrain. Buyers can issue RFQs, compare landed prices and lock multi-month supply contracts directly with manufacturers, bypassing layered intermediaries that typically add 6 to 12 percent to procurement costs.

Conclusion

The GCC cement story in 2026 is no longer about whether demand will materialise, it has, and the USD 9.1 billion market value confirms it. The strategic question for procurement leaders is how to operate inside a market where capacity utilisation is high, freight is volatile, carbon specifications are tightening and the megaproject pipeline keeps expanding through 2031 and beyond. Buyers who lengthen contracts, diversify within country, build freight contingency into landed cost and engage suppliers on low-carbon options now will spend the rest of the decade ahead of their competition rather than scrambling behind it. The data points one way; the procurement playbook needs to move with it.