In This Analysis

- How Hormuz Disruption Cracked GCC Pharma Supply Chains

- NUPCO, MiS Scores, and the Saudi Localization Mandate

- UAE's Parallel Track: MOHAP, Free Zones, and API Attraction

- The Biosimilar Boom: Where Buyers Must Act Now

- Qualifying as a GCC Pharma Supplier in 2026

- The Procurement Playbook: Building Resilience for 2027

The numbers that hit Gulf procurement desks in early March 2026 were stark. Commercial cargo through the Strait of Hormuz — a corridor that normally moves a meaningful share of the world's pharmaceutical raw materials and finished goods — had dropped to roughly 10% of pre-war levels. At the same time, air-cargo capacity across major Gulf hubs collapsed by 79% in the space of five days. For any GCC pharmaceutical buyer managing a live hospital formulary, that combination wasn't an abstract geopolitical event. It was a formulary gap that needed filling by Tuesday.

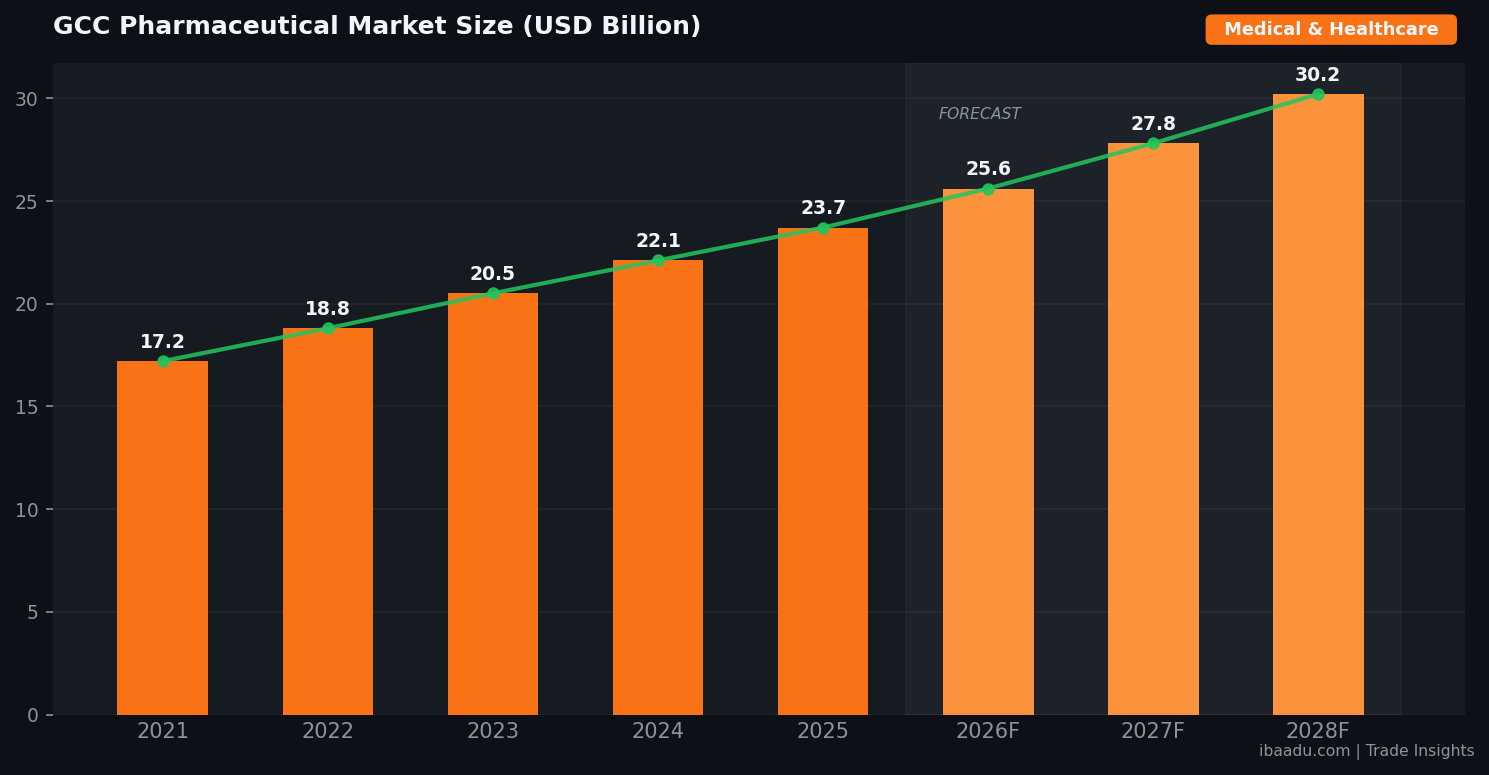

The GCC pharmaceutical market is worth approximately $23.7 billion as of 2026, according to data from PharmaKnowl Consulting and industry benchmarking aggregated by the Gulf Business Council. What makes it uniquely exposed is the import structure: somewhere between 80% and 85% of pharmaceutical consumption across the six GCC states arrives from outside the region — principally from India, China, and Western Europe, and predominantly via the Strait of Hormuz or the Gulf's major air hubs. When both of those channels seized up simultaneously, procurement teams discovered just how thin their safety margins actually were.

This analysis is for procurement managers, supply chain directors, and vendor representatives who need to understand not just what happened, but what it means for sourcing strategy through 2027.

How Hormuz Disruption Cracked GCC Pharma Supply Chains

Procurement professionals who've worked the Gulf for more than a decade know the Strait of Hormuz has always been the single point of failure that no one in government wanted to formally acknowledge. That's changed now. Baker McKenzie's May 2026 analysis of Gulf pharmaceutical supply chains under geopolitical pressure put the risk in plain regulatory language: the region's structural import dependency means that any prolonged corridor closure creates "critical shortage thresholds" within 30 to 60 days for certain therapeutic categories.

The therapeutic categories hit hardest in the Q1 2026 disruption were predictable in retrospect: injectable biologics requiring cold-chain integrity across long-haul routes, oncology APIs sourced from specialised Indian and Chinese manufacturers, and ICU consumables that hospital procurement teams had never prioritised for local buffer stock because, historically, they'd always arrived on time.

What wasn't predictable — or at least, wasn't widely modelled — was the speed of the air-freight collapse. When Gulf air hubs began operating at significantly reduced capacity between late February and early March 2026, pharmaceutical importers expecting to pivot from sea freight to air freight found that emergency premium booking had already consumed most available belly-cargo space. The result was a cascading shortage that hit secondary-tier GCC markets — Bahrain, Kuwait, Oman — harder than UAE and Saudi Arabia, simply because smaller markets had thinner distributor stockholding.

The lesson for procurement teams isn't to stock six months of everything. It's to know, with specificity, which items in your formulary have single-source supply chains, and to have alternate-supplier qualification already completed before the disruption arrives. The buyers who managed Q1 2026 best weren't those with the biggest warehouses — they were those with the shortest supplier qualification lead times.

At ibaadu.com, we've seen a significant uptick in procurement teams from GCC hospitals and healthcare groups searching for verified alternative suppliers specifically for injectable APIs and branded generics. The shift from reactive emergency sourcing to proactive alternate-supplier registration is the defining procurement behaviour change of 2026 in this sector.

NUPCO, MiS Scores, and the Saudi Localization Mandate

If the Hormuz disruption provided the crisis narrative, Saudi Arabia's procurement framework provided the structural response. And the response, frankly, is more aggressive than most international suppliers anticipated.

NUPCO — the National Unified Procurement Company, which handles pharmaceutical procurement for Saudi Arabia's government health system — has embedded a 15% "Made in Saudi" (MiS) localization score directly into its 2026 tender evaluation methodology. That 15% is not a preference signal or a tie-breaker. In competitive tendering, it's frequently the margin that determines the winning bid. International suppliers offering clinically equivalent products at equivalent prices will lose to a locally manufactured alternative every time, because the MiS score pushes the locally manufactured option over the threshold.

The broader Vision 2030 target is for 80% of pharmaceutical consumption to be locally manufactured by 2030. As of 2026, Saudi Arabia has approximately 40 operational pharmaceutical factories covering an estimated 36% of market demand, with local production growing at 5% annually and pharmaceutical exports already exceeding SAR 1.5 billion (roughly $400 million USD). The math on the gap between 36% and 80% is what's driving the intensity of the current incentive structure.

For international pharmaceutical manufacturers watching this from outside the region: the qualification requirement is real and the timeline is accelerating. Only SFDA-approved, locally manufactured products qualify for NUPCO's national tenders and long-term framework agreements. The SFDA approval process, while rigorous, is navigable — particularly for manufacturers who engage early and correctly. The mistake most international suppliers make is treating SFDA registration as an afterthought to commercial discussions, rather than as the commercial prerequisite it's become.

Toll-manufacturing arrangements with established Saudi pharmaceutical groups — where an international formulation is produced at a licensed Saudi facility under co-branding or OEM arrangements — are increasingly the route to market for mid-sized international suppliers that can't justify a full greenfield investment. The economics work on volumes above roughly 500,000 units per year for solid-dosage forms, and on significantly lower volumes for specialty injectables where the unit economics are more favourable.

Procurement teams at Saudi government hospitals and private health systems need to understand the flip side: domestically manufactured alternatives they've never evaluated are now competitive for tender positions they previously assumed were held by international incumbents. That should prompt a formulary review for any category where you haven't re-tendered in the past 18 months.

You can find verified pharmaceutical vendors registered on ibaadu across the medical equipment and consumables categories, with many already holding SFDA and MOHAP registration documentation.

UAE's Parallel Track: MOHAP, Free Zones, and API Attraction

The UAE's approach to pharmaceutical supply-chain resilience runs on a parallel but distinct track from Saudi Arabia's. Where Saudi Arabia's primary lever is the NUPCO tender framework and Vision 2030 localization mandates, the UAE is using its free-zone architecture and regulatory infrastructure to attract pharmaceutical manufacturing capital directly.

Dubai Science Park, Khalifa Industrial Zone Abu Dhabi (KIZAD), and the Dubai Multi Commodities Centre (DMCC) have all expanded pharmaceutical and life-sciences clustering programmes through 2025 and 2026. The DMCC's pharmaceutical-grade storage facilities have seen occupancy rates climb significantly as regional distributors consolidated inventory positions in response to the supply-chain disruptions earlier this year. Companies that would previously have held minimal UAE-based stock because of the cost of free-zone warehousing are now running carrying-cost calculations that look very different once the alternative is a formulary gap during a Hormuz disruption.

The UAE's MOHAP (Ministry of Health and Prevention) registration pathway, while rigorous, is typically faster than SFDA for products already approved by a stringent reference authority (US FDA, EMA, or Health Canada). For international manufacturers looking at GCC market entry, UAE registration followed by SFDA registration — using the UAE dossier as a reference point — is frequently the most efficient sequencing.

One dynamic that surprises even experienced Gulf procurement professionals: the UAE's free-zone pharmaceutical re-export model has quietly become a critical buffer mechanism for the broader GCC. When Oman, Kuwait, or Bahrain healthcare systems face acute shortages, a significant portion of the emergency supply often moves from UAE free-zone stockholding into those markets. This makes UAE-based distributors and free-zone logistics operators structurally important to regional pharmaceutical procurement stability in ways that don't appear in any country-level supply-chain analysis.

For healthcare procurement teams across the GCC, the practical implication is to review whether your distributor has meaningful UAE free-zone inventory as a buffer position, or whether their stockholding model leaves you fully exposed to the primary import corridor.

The Biosimilar Boom: Where Buyers Must Act Now

The structural shift happening in GCC pharmaceutical procurement that most people are underestimating is biosimilars. Not because the concept is unfamiliar — every procurement director in the region knows biosimilars are coming — but because the pace of market entry and the pricing dynamics are moving faster than most formulary committees have updated their policies to accommodate.

Biosimilar growth in the Middle East is currently tracking at 15–20% CAGR, according to industry data from GlobalNewswire and Mordor Intelligence. The MEA pharmaceutical contract manufacturing market reached $3.93 billion in 2026, with biologic manufacturing increasingly shifting into regional facilities. Oncology and autoimmune biosimilars are the leading therapeutic areas.

The financial opportunity for buyers is significant. A GCC hospital formulary that has not yet evaluated biosimilar alternatives for its top-five biologic spend categories is almost certainly leaving 20–35% cost savings on the table — savings that, at current biologic price levels, translate to millions of dirhams or riyals annually for a major health system. The procurement question isn't whether to source biosimilars; it's which biosimilars have adequate regional pharmacovigilance data and sufficient supply-chain reliability for formulary inclusion.

The supply-chain reliability question is real and shouldn't be dismissed. Several biosimilar manufacturers that entered the GCC market between 2022 and 2024 have struggled with batch-release consistency and cold-chain compliance at the regional distribution level. Before switching a high-volume biologic to a biosimilar, procurement teams should require: three consecutive batch release reports, a demonstrated cold-chain audit for UAE or Saudi distribution, and a clear contingency plan if supply is interrupted. Don't accept "we'll manage it" as an answer — get the contingency supplier pre-qualified before you switch the primary.

High-potency APIs (HPAPIs) represent another fast-moving category. Growing at 9–12% annually in the Middle East as oncology pipelines advance, HPAPIs require specialised containment manufacturing that few regional facilities currently offer. For procurement teams sourcing for oncology centres or specialty hospitals, maintaining at least two pre-qualified international HPAPI suppliers — with one holding a confirmed UAE free-zone stock position — is worth the cost of the additional qualification work.

Qualifying as a GCC Pharma Supplier in 2026

For suppliers looking to enter or expand their GCC pharmaceutical market position, the qualification landscape in 2026 is more structured than it's ever been — which is both an opportunity and a barrier depending on how prepared you are.

The GCC Health Council's push for a unified pharmaceutical directory across the six member states is the most significant structural change in regional procurement governance. The council's unified directory aims to harmonise product specifications, pricing reference points, and supplier qualification standards. For suppliers, a unified registration could eventually replace the current country-by-country registration process — but don't wait for full implementation. The individual country registration requirements (SFDA, MOHAP, Kuwait MOH, Qatar MOPH) remain the operative qualifying conditions for 2026 tenders.

The baseline qualification requirements haven't changed in principle, but the enforcement rigour has increased substantially post-disruption:

For Saudi Arabia (NUPCO and private sector): SFDA Good Manufacturing Practice (GMP) approval is mandatory. The MiS localization score applies to national tenders. For foreign manufacturers, either direct SFDA registration or a licensed Saudi manufacturing partnership is required to be competitive.

For UAE (MOHAP and private hospital procurement): MOHAP product registration plus a licensed UAE-based distributor. For free-zone stockholding, DAFZA or JAFZA registration is standard. Products registered by stringent reference authorities benefit from an expedited pathway.

For Qatar, Oman, Kuwait, Bahrain: Individual ministry of health registrations apply, but practical market access usually runs through a registered local distributor or commercial agent. The SEZAD free zone in Duqm (Oman) is emerging as a pharmaceutical warehousing hub for Indian Ocean trade routes as an alternative to Gulf corridor dependence.

ibaadu.com maintains a verified directory of pharmaceutical suppliers and medical equipment vendors across the GCC, including registration status and distribution network details. It's the fastest way for procurement teams to identify pre-qualified alternatives, and for suppliers to reach active GCC buyers directly.

The Procurement Playbook: Building Resilience for 2027

The Q1 2026 disruption has effectively compressed what would have been a five-year supply-chain transformation into an 18-month forced adaptation. Procurement teams that use the pressure productively will emerge with meaningfully more resilient supply chains. Those that treat it as a temporary crisis to be managed until the corridor reopens will be in the same position the next time it happens — and they should assume there will be a next time.

Dual-source qualification is the single highest-return investment a pharmaceutical procurement team can make right now. For every top-50 spend item by value, you should have a pre-qualified alternative supplier on file — not a supplier you've identified theoretically, but one that's completed your quality questionnaire, holds appropriate regulatory approvals for your market, and has confirmed they can supply at your volumes within a 30-day notice period. The qualification work is time-consuming but it's not complicated. It just requires prioritisation.

Buffer stock policy needs to be recalibrated based on corridor risk, not historical delivery reliability. The historical reliability data from 2018–2024 is not a useful guide for 2025–2027 planning. A category that previously warranted four weeks of buffer stock based on a three-day lead time from a Jebel Ali warehouse may now warrant eight weeks of buffer, because the corridor risk has fundamentally changed.

Regional re-export monitoring is worth building into your supply intelligence. If you're sourcing for a smaller GCC market and your UAE distributor is also supplying the UAE market from the same stock position, you have an invisible exposure: in a shortage situation, the UAE domestic demand may take priority over your re-export allocation. Understanding your distributor's contractual commitments across their portfolio is an underappreciated dimension of pharmaceutical supply-chain risk in the Gulf.

Can't afford to build a dedicated supply-chain intelligence function? Connect directly with verified suppliers on ibaadu.com or reach our procurement matchmaking team on WhatsApp — we can help you identify pre-qualified alternative suppliers for specific formulary categories quickly, without the overhead of a full procurement transformation project.

Find Verified Pharmaceutical Suppliers Across the GCC

ibaadu connects healthcare procurement teams with SFDA and MOHAP-registered manufacturers, distributors, and medical equipment vendors across the Gulf. Free access — no intermediary fees.

Browse Verified Suppliers →Frequently Asked Questions

How is the Strait of Hormuz disruption affecting GCC pharmaceutical procurement in 2026?

With commercial cargo through the Strait of Hormuz at roughly 10% of pre-war levels as of early 2026, GCC pharmaceutical buyers faced severe API and finished-goods shortages. Air freight capacity in the Gulf dropped 79% during the February–March 2026 peak disruption period, forcing procurement teams to activate emergency stock protocols and accelerate local sourcing agreements. The sectors hit hardest were injectable biologics, oncology APIs, and ICU consumables with single-source supply chains.

What is NUPCO's MiS localization score and how does it affect supplier selection?

NUPCO now embeds a 15% Made in Saudi (MiS) localization score into its 2026 tender evaluation framework. Only SFDA-approved, locally manufactured products qualify for national tenders and long-term framework agreements. For international suppliers, local manufacturing partnerships or toll-manufacturing arrangements in Saudi Arabia have become competitively essential — not optional.

Which pharmaceutical categories offer the largest procurement opportunity in the GCC right now?

Biosimilars (15–20% CAGR), oncology APIs, and generic solid-dosage forms represent the fastest-growing procurement categories in 2026. The MEA contract manufacturing market reached $3.93 billion. Hospital consumables, cold-chain biologics, and SFDA-approved finished pharmaceuticals for government tenders are the most actively tendered categories across the GCC right now.

How can international pharma suppliers qualify for GCC government procurement tenders?

International pharma suppliers need SFDA approval for Saudi tenders and MOHAP registration for UAE procurement. Partnership with a licensed local distributor, registration on the GCC Health Council's unified pharmaceutical directory, and ISO/GMP certification are baseline requirements. ibaadu.com connects verified international manufacturers with licensed GCC distributors and procurement teams directly — contact us on WhatsApp at +971585978602.

The GCC pharmaceutical supply chain is going through a structural reset that will take 18–24 months to stabilise. The procurement teams and suppliers that act on dual-source qualification, local manufacturing partnerships, and buffer stock recalibration now will be significantly better positioned when the next corridor disruption arrives — and in 2026, it's safe to assume they will.

ibaadu.com is the B2B marketplace built for this moment: a verified directory of GCC-registered pharmaceutical manufacturers, distributors, and medical equipment suppliers, with direct buyer-to-supplier connection. No intermediary markups. No cold-calling directories that haven't been updated since 2022.

Ready to qualify alternative suppliers for your formulary? Our procurement team is available on WhatsApp for direct, fast-response sourcing support.

💬 WhatsApp Our Procurement TeamBrowse All Verified Suppliers on ibaadu.com →